Credit Guarantee Scheme for MSMEs: Complete Guide to CGTMSE 2026

Introduction to Credit Guarantee Schemes for Indian MSMEs in 2026

Credit Guarantee Schemes for Indian MSMEs are government-backed initiatives designed to provide collateral-free or third-party guarantee-free credit facilities from financial institutions. These schemes reduce the risk perception for lenders, thereby encouraging banks and NBFCs to extend loans to micro, small, and medium enterprises, which often lack the tangible assets required for traditional collateral.

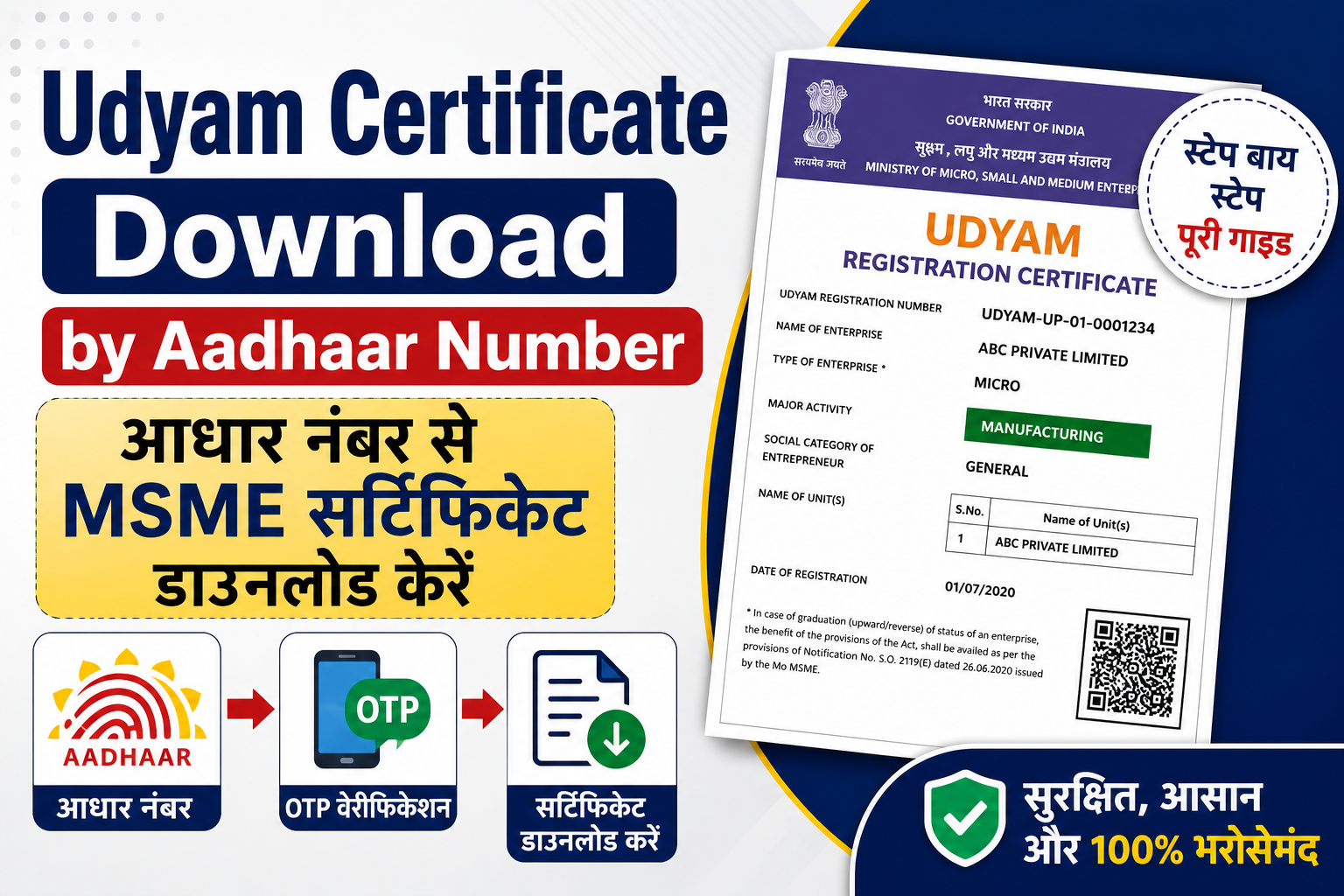

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

In the financial year 2025-26, Micro, Small, and Medium Enterprises (MSMEs) continue to be the backbone of India's economy, contributing significantly to employment generation and GDP. However, accessing timely and adequate credit, especially without requiring collateral, remains a critical challenge for many. Recognising this, the Indian government has implemented various credit guarantee schemes to bridge this financing gap and bolster the growth of the MSME sector.

The landscape for MSME finance in India has significantly evolved, driven by policy reforms aimed at enhancing credit flow. Credit Guarantee Schemes play a pivotal role by assuring lenders against a specified portion of the default risk, thereby incentivising them to lend more freely to MSMEs. This mechanism is crucial for startups and smaller enterprises that may not possess the conventional collateral often demanded by banks. The Micro, Small and Medium Enterprises Development (MSMED) Act, 2006, forms the legislative framework for the development and regulation of MSMEs, while subsequent initiatives like Udyam Registration, introduced via Gazette Notification S.O. 2119(E) dated 26 June 2020, have streamlined the identification and formalisation of these businesses, making them eligible for a wider array of benefits.

One of the flagship initiatives in this regard is the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), managed jointly by the Ministry of MSME and SIDBI. Launched to make collateral-free credit available to the micro and small enterprise sector, CGTMSE has significantly expanded its reach. As of 2026, it offers guarantees for credit facilities up to Rs 5 crore per eligible MSME, covering both term loans and working capital. The scheme has been instrumental in supporting lakhs of micro and small units across the country, mitigating the hesitation of lenders by sharing the credit risk. The guarantee fee structure, ranging from 0.37% to 1.35%, and additional benefits for categories like women entrepreneurs or units in the North-East, further enhance its accessibility (sidbi.in).

Beyond CGTMSE, other government initiatives also address the credit needs of smaller businesses. The Pradhan Mantri MUDRA Yojana (PMMY), for instance, provides collateral-free loans up to Rs 10 lakh to non-corporate, non-farm small/micro enterprises. Divided into Shishu (up to Rs 50,000), Kishore (Rs 50,001 to Rs 5 lakh), and Tarun (Rs 5 lakh to Rs 10 lakh) categories, MUDRA loans facilitate access to finance for a vast segment of the informal economy, encouraging entrepreneurship and self-employment (mudra.org.in). The Udyam Registration is increasingly becoming a prerequisite for accessing many of these schemes, consolidating MSME data and simplifying the application process for various government benefits (udyamregistration.gov.in).

These credit guarantee schemes are not merely financial tools; they are powerful enablers of economic growth and social inclusion. By reducing reliance on physical collateral, they democratise access to finance, empowering a new generation of entrepreneurs and fostering innovation within the MSME sector, thereby aligning with India's broader economic development goals.

Key Takeaways

- Credit Guarantee Schemes aim to facilitate collateral-free loans for Indian MSMEs, mitigating lender risk.

- The MSMED Act, 2006, provides the foundational legal framework for MSME development in India.

- Udyam Registration, introduced in 2020, is crucial for formalising MSMEs and accessing government benefits.

- CGTMSE, managed by the Ministry of MSME and SIDBI, offers credit guarantees up to Rs 5 crore for eligible micro and small enterprises.

- Pradhan Mantri MUDRA Yojana (PMMY) provides collateral-free loans up to Rs 10 lakh under Shishu, Kishore, and Tarun categories.

- These schemes are vital for promoting entrepreneurship and ensuring financial inclusion for a large segment of India's business landscape.

What is CGTMSE (Credit Guarantee Trust for Micro and Small Enterprises)?

The Credit Guarantee Trust for Micro and Small Enterprises (CGTMSE) is a scheme launched by the Government of India and SIDBI to provide credit guarantees to financial institutions for collateral-free credit facilities extended to Micro and Small Enterprises (MSMEs). It aims to ensure that viable MSME projects do not fail due to lack of collateral, thereby promoting entrepreneurship and economic growth.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

Micro and Small Enterprises (MSMEs) form the backbone of the Indian economy, contributing significantly to GDP, exports, and employment generation. However, a persistent challenge for these enterprises, especially startups and first-generation entrepreneurs, has been accessing formal credit due to a lack of tangible collateral. In 2025-26, bridging this credit gap remains a critical focus for fostering robust economic development.

To address this crucial issue, the Ministry of Micro, Small & Medium Enterprises (MoMSME), Government of India, and Small Industries Development Bank of India (SIDBI) jointly established the Credit Guarantee Trust for Micro and Small Enterprises (CGTMSE) in 2000. The primary objective of the CGTMSE scheme is to make collateral-free credit available to the micro and small enterprise sector. Under this scheme, the Trust acts as a third-party guarantor to lenders, assuring them a certain percentage of the credit facility in case of default by the MSME borrower.

The scheme essentially mitigates the risk for banks and financial institutions, encouraging them to lend more freely to eligible MSMEs without demanding primary or collateral security. This mechanism has been instrumental in expanding access to institutional credit, particularly for micro-enterprises and those in underserved regions. As per the scheme guidelines, eligible credit facilities, including both term loans and working capital, can receive guarantee coverage of up to ₹5 crore per MSME unit. This substantial coverage aims to support various stages of business growth, from initial setup to expansion and modernisation.

CGTMSE charges an annual guarantee fee from the lending institutions, which typically ranges between 0.37% to 1.35% of the guaranteed amount. This fee structure is designed to be affordable while ensuring the sustainability of the Trust. Notably, special provisions are often incorporated to encourage lending to specific categories, such as women entrepreneurs and MSMEs located in the North Eastern Region, where enhanced guarantee coverage or concessional terms may apply, including an additional 5% coverage in certain cases to further incentivise lenders. The operational framework of CGTMSE is regularly reviewed and updated to align with evolving needs of the MSME sector, ensuring its continued relevance and effectiveness in the Indian financial landscape. For detailed terms, financial institutions refer to circulars published by SIDBI (sidbi.in) under the scheme.

Key Takeaways

- CGTMSE was established in 2000 by MoMSME and SIDBI to facilitate collateral-free loans for MSMEs.

- The scheme provides credit guarantees to lenders, covering a portion of the loan in case of borrower default.

- MSMEs can avail collateral-free credit facilities, including term loans and working capital, up to ₹5 crore under CGTMSE.

- Lending institutions pay an annual guarantee fee to CGTMSE, typically between 0.37% and 1.35% of the guaranteed amount.

- Enhanced guarantee coverage is often provided for loans to women entrepreneurs and units in the North Eastern Region.

Who is Eligible for CGTMSE Credit Guarantee Coverage

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) provides credit guarantee coverage primarily to Micro and Small Enterprises (MSEs) that hold a valid Udyam Registration. Eligibility extends to both new and existing enterprises across manufacturing, service, and specified trade activities, receiving term loans and working capital facilities up to ₹5 crore from eligible financial institutions. Special benefits, such as reduced guarantee fees, are often extended to women entrepreneurs and units located in aspirational districts or the North-Eastern Region.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

Updated 2025-2026: CGTMSE guidelines continue to evolve, with special provisions for women entrepreneurs and units in aspirational districts, reflecting the ongoing focus on inclusive growth and enhanced credit access.

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) stands as a cornerstone in facilitating collateral-free credit to the Micro and Small Enterprises (MSEs) sector in India. In the fiscal year 2025-26, the scheme continues to empower a diverse range of enterprises, particularly focusing on those traditionally underserved by formal credit channels, by reducing the risk perception for lenders. Understanding the precise eligibility criteria is crucial for enterprises seeking to avail its benefits, which include loans up to ₹5 crore without requiring collateral or third-party guarantees from scheduled commercial banks, select regional rural banks, and other approved financial institutions.

To qualify for CGTMSE coverage, an enterprise must primarily be classified as a Micro or Small Enterprise as per the MSMED Act, 2006, and possess a valid Udyam Registration Certificate. This registration, introduced by Gazette Notification S.O. 2119(E) dated 26 June 2020, replaced the erstwhile Udyog Aadhaar and is a prerequisite for most MSME-related schemes. The scheme is designed to cover a broad spectrum of economic activities, encompassing both manufacturing and service sectors. Notably, recent amendments have also extended eligibility to certain retail and wholesale trade activities, thereby broadening the scheme's reach and impact across various business segments.

The type of credit facility is also a key determinant. CGTMSE covers both term loans and working capital facilities, or a combination thereof. The maximum eligible loan amount for coverage under the scheme is ₹5 crore. This limit allows a significant portion of the MSE sector to access substantial credit without the burden of providing collateral, which is often a major hurdle for new and growing businesses. Furthermore, the scheme actively promotes inclusive growth by offering enhanced guarantee coverage and/or reduced annual guarantee fees for specific categories of borrowers, such as women entrepreneurs and enterprises located in the 112 Aspirational Districts or the North-Eastern Region, demonstrating the government's commitment to supporting vulnerable segments and backward regions.

CGTMSE Eligibility Overview

| Criterion | Details |

|---|---|

| Enterprise Type | Micro and Small Enterprises (MSEs) engaged in manufacturing, services, and eligible retail/wholesale trade activities. Medium Enterprises are not covered. |

| Registration Status | Must possess a valid Udyam Registration Certificate, as specified by Gazette Notification S.O. 2119(E) dated 26 June 2020. |

| Credit Facility Type | Term loans, working capital facilities, or composite loans. |

| Loan Amount Limit | Up to ₹5 crore per borrowing unit. |

| Lending Institutions | All Scheduled Commercial Banks (SCBs), select Regional Rural Banks (RRBs), Small Industries Development Bank of India (SIDBI), and other eligible financial institutions. |

| Borrower Status | Applicable for both new and existing enterprises. |

| Special Categories | Women entrepreneurs, units in Aspirational Districts, and North-Eastern Region benefit from higher guarantee coverage and/or lower guarantee fees. |

Source: SIDBI (sidbi.in), MSME Ministry (msme.gov.in)

Key Takeaways

- CGTMSE primarily covers Micro and Small Enterprises (MSEs) registered with Udyam, excluding Medium Enterprises.

- Both manufacturing and service sector enterprises, along with specified retail and wholesale trade activities, are eligible for coverage.

- The scheme extends to term loans and working capital facilities up to a maximum of ₹5 crore.

- Eligible loans must be disbursed by Scheduled Commercial Banks, select Regional Rural Banks, and other approved financial institutions.

- Special provisions, including reduced guarantee fees (e.g., 0.37-1.35% base fee, extra 5% for women/NE as per SIDBI), are available for women entrepreneurs and units in Aspirational Districts or the North-Eastern Region.

- The objective is to enable collateral-free access to institutional credit, supporting growth and innovation within the MSME sector.

Step-by-Step Process to Apply for CGTMSE Guarantee

The application for CGTMSE guarantee is initiated by the eligible lending institution after sanctioning a collateral-free loan to an MSME. The MSME first applies for a term loan or working capital facility from a bank or financial institution, which then processes the loan application and, if approved, applies for the CGTMSE cover on behalf of the borrower through the SIDBI portal.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

In the fiscal year 2025-26, the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) continues to be a pivotal scheme, having supported numerous MSMEs with collateral-free credit. Entrepreneurs seeking financial assistance under this scheme must understand that the application process is primarily facilitated by their lending institution. The scheme aims to bolster the credit flow to the MSME sector by mitigating the risk for banks.

The application for a CGTMSE guarantee is an indirect process for the MSME borrower, as the guarantee is provided to the eligible lending institution. The steps below outline how an MSME can effectively avail a loan covered by the CGTMSE scheme.

- MSME Loan Application: The first step for an MSME is to prepare a robust business plan and apply for a term loan or working capital facility from an eligible Member Lending Institution (MLI). These MLIs typically include public sector banks, private sector banks, foreign banks, regional rural banks, and select financial institutions that are registered with CGTMSE. The loan amount can be up to Rs 5 crore, as specified by the scheme guidelines.

- Lender's Due Diligence: The MLI will conduct its standard due diligence, credit appraisal, and sanction the loan based on the project's viability and the borrower's creditworthiness. It is crucial for the MSME to meet the lender's internal credit policies and be classified as a Micro or Small Enterprise as per the criteria laid out in Gazette Notification S.O. 2119(E) dated 26 June 2020 (Micro: ≤ ₹1 Cr investment & ₹5 Cr turnover; Small: ≤ ₹10 Cr investment & ₹50 Cr turnover).

- Application for CGTMSE Cover by Lender: Once the loan is sanctioned and disbursed, the MLI will initiate the application for the CGTMSE guarantee cover on behalf of the MSME. The bank accesses the online portal of the Credit Guarantee Fund Trust for Micro and Small Enterprises (sidbi.in) to submit the necessary details and documents. This typically occurs within 90 days of the loan sanction or first disbursement, whichever is earlier.

- Payment of Guarantee Fee: The MLI pays the annual guarantee fee to CGTMSE. This fee varies, generally ranging from 0.37% to 1.35% of the guaranteed amount, depending on the loan amount and category of the borrower. It's important to note that this fee is often passed on to the borrower by the bank. For loans to women entrepreneurs or those located in the North Eastern Region, an additional 5% guarantee coverage is provided, and the guarantee fee might be lower, enhancing access to credit in these priority sectors.

- Issuance of Guarantee Confirmation: Upon successful submission of the application and payment of the guarantee fee, CGTMSE processes the request and issues a Guarantee Confirmation to the MLI. This confirmation signifies that the loan is now covered under the scheme, providing comfort to the lender against potential defaults. The entire process is streamlined to ensure quick processing, typically within a few days of the bank's submission.

- Ongoing Compliance: For the guarantee to remain active, the MLI and the MSME must adhere to the terms and conditions outlined by CGTMSE. This includes timely repayment of the loan by the MSME and regular payment of the annual guarantee fee by the MLI. Any non-compliance could lead to the revocation of the guarantee cover.

Understanding that the lender is the primary applicant for CGTMSE cover enables MSMEs to focus on preparing a robust financial proposal and maintaining a strong relationship with their bank. The scheme truly democratises credit access by removing the need for collateral, which has historically been a significant barrier for micro and small enterprises.

Key Takeaways

- The CGTMSE application is initiated by the eligible lending institution (MLI), not directly by the MSME.

- MSMEs must first secure a collateral-free loan from a bank or financial institution, which acts as the MLI.

- The loan amount eligible for CGTMSE cover can extend up to Rs 5 crore.

- MLIs apply for the guarantee cover and pay an annual fee to CGTMSE, typically between 0.37% and 1.35% of the guaranteed amount.

- Women entrepreneurs and MSMEs in the North Eastern Region receive enhanced benefits, including potentially lower fees and higher coverage.

- Maintaining timely loan repayments is crucial for the continuous validity of the CGTMSE guarantee.

Required Documents and Prerequisites for CGTMSE Application

To apply for the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) scheme, businesses primarily require a valid Udyam Registration Certificate, identity and address proofs of proprietors/partners/directors, business financial statements (ITR, bank statements), and a detailed project report or business plan. The application is facilitated through eligible Member Lending Institutions (MLIs), which assist in collating necessary documentation for loan sanction and guarantee cover.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

Securing collateral-free loans for Micro and Small Enterprises (MSEs) under the CGTMSE scheme is a significant boost for growth, with the scheme guaranteeing loans up to ₹5 crore as of 2025-26. A meticulous approach to gathering the necessary documents and fulfilling prerequisites is crucial for a smooth application process. Proper documentation ensures that the lending institution can accurately assess the business's viability and eligibility for the guarantee cover provided by the Trust.

The application for CGTMSE cover is not a direct process with CGTMSE itself but is integrated into the loan application process with a Member Lending Institution (MLI), such as commercial banks, regional rural banks, and select financial institutions. The MLI scrutinizes the business proposal and the applicant's credentials before forwarding the request for CGTMSE cover. Therefore, the documents required are primarily those needed for a standard business loan, with an emphasis on the MSME status.

Key Prerequisites for CGTMSE Eligibility

Before initiating the loan application with an MLI, certain fundamental prerequisites must be met to ensure eligibility for CGTMSE cover:

- Udyam Registration: This is the most crucial requirement. Only enterprises formally registered as Micro or Small under the Udyam Registration portal are eligible for CGTMSE benefits. The Udyam Registration Certificate serves as definitive proof of MSME status as per Gazette Notification S.O. 2119(E) dated 26 June 2020.

- Loan Type: The scheme covers term loans and/or working capital facilities sanctioned by eligible MLIs without any collateral security and/or third-party guarantee. The maximum guarantee cover is up to ₹5 crore per eligible MSE.

- Business Viability: The MLI will assess the project's economic viability and the promoter's capability to repay the loan. A sound business plan or project report is vital in this assessment.

- Creditworthiness: While collateral is not required, a clean credit history of the promoters and the business (if existing) is generally preferred by MLIs.

It is important to note that the specific list of documents may vary slightly based on the lending institution's internal policies and the nature of the business and loan. However, the core set of documents remains largely consistent. For informal micro units without a PAN or GSTIN, the Udyam Assist Platform, launched in January 2023, facilitates Udyam Registration for access to such schemes.

Essential Documents for CGTMSE Application

| Document Category | Specific Documents Required | Purpose / Details |

|---|---|---|

| Business Entity Proof | Udyam Registration Certificate | Mandatory proof of MSME status (udyamregistration.gov.in) |

| PAN Card of the Enterprise | Tax identity of the business | |

| Partnership Deed / MOA & AOA / LLP Agreement | Legal structure proof for Partnership, Company, LLP | |

| Certificate of Incorporation (for Companies/LLPs) | Official registration proof from MCA (mca.gov.in) | |

| Shop & Establishment Act Registration | Mandatory for retail/service businesses (state-specific) | |

| Identity & Address Proof (Promoters/Partners/Directors) | PAN Card | Individual tax identity |

| Aadhaar Card | Address and identity proof | |

| Proof of Residence (Electricity bill, Passport, Voter ID) | Verification of promoter's address | |

| Financial Documents | Bank Statements (past 6-12 months) | Operational cash flow and transaction history |

| Income Tax Returns (ITR) for past 2-3 years (Business & Promoters) | Financial health and income history | |

| Project Report / Business Plan | Detailed outline of business, financial projections, repayment plan | |

| Provisional/Audited Financial Statements (Balance Sheet, P&L) | For existing businesses to assess financial performance | |

| GST Registration Certificate & Returns (if applicable) | Proof of GST compliance and turnover | |

| Loan Specific Documents | Duly filled Loan Application Form | Provided by the Member Lending Institution (MLI) |

| Quotation/Estimate for machinery/assets (for term loan) | Details of proposed investment | |

| Stock & Debtors Statement (for working capital) | For assessment of working capital needs | |

| Consent for CIBIL/Credit Score check | Required for assessing creditworthiness |

Source: sidbi.in, msme.gov.in

Key Takeaways

- Udyam Registration is the foundational prerequisite for CGTMSE scheme eligibility, establishing MSME status.

- The CGTMSE application is integrated into the loan process with Member Lending Institutions (MLIs), not a direct application.

- Essential documents include business registration proofs, promoter's identity and address proofs, and comprehensive financial records.

- A well-prepared project report or business plan is crucial for new ventures or expansions to demonstrate viability and repayment capacity.

- While CGTMSE offers collateral-free loans, a clean credit history of the promoters remains a key factor for MLIs during assessment.

- The maximum guarantee cover under the scheme for eligible MSEs is up to ₹5 crore, supporting both term loans and working capital.

Key Benefits and Coverage Under CGTMSE Scheme

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) scheme provides collateral-free or third-party guarantee-free credit facilities up to Rs 5 crore to eligible Micro and Small Enterprises (MSMEs). This significantly reduces the risk for lending institutions and enhances access to formal credit for entrepreneurs who lack tangible collateral.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

Access to timely and affordable credit without collateral remains a significant challenge for many Micro and Small Enterprises (MSMEs) in India. The CGTMSE scheme, a flagship initiative by the Ministry of MSME and SIDBI, was designed precisely to address this gap. By offering a guarantee cover to Member Lending Institutions (MLIs), it encourages banks and financial institutions to extend credit to MSMEs, including new ventures, without demanding traditional collateral. This mechanism significantly streamlines credit access for the 2025-26 fiscal year, fostering entrepreneurship and economic growth across various sectors.

The primary goal of CGTMSE is to facilitate a robust flow of institutional credit to the MSME sector by mitigating the lending risk for financial institutions. This ensures that deserving businesses are not hindered by a lack of tangible assets for collateral. The scheme's comprehensive coverage extends to both term loans for asset acquisition and working capital facilities crucial for day-to-day operations, thereby offering complete financial support.

Core Benefits of CGTMSE

- Collateral-Free Credit: The most significant advantage is the provision of loans up to Rs 5 crore without any collateral or third-party guarantee, making credit accessible to a broader base of entrepreneurs (sidbi.in).

- Enhanced Access to Finance: By absorbing a substantial portion of the credit risk, the scheme motivates MLIs to lend more readily to MSMEs, improving their creditworthiness in the eyes of lenders.

- Reduced Borrowing Hurdles: Eliminating the need for collateral significantly simplifies the loan application process and reduces the time and effort required to secure financing.

- Incentives for Specific Categories: The scheme offers higher guarantee coverage and/or lower fees for loans extended to women entrepreneurs, units located in the North Eastern Region (including Sikkim), and enterprises owned by SC/ST individuals, promoting inclusive growth as per Ministry of MSME guidelines (msme.gov.in).

- Comprehensive Coverage: It supports a wide range of MSME activities, covering both manufacturing and service enterprises, along with specific retail trade activities, ensuring diverse sector participation.

Coverage Details Under CGTMSE

The extent of guarantee cover provided under CGTMSE varies based on the loan amount and the category of the borrower. This structured approach ensures optimal risk sharing between the Trust and the MLIs:

- Micro Enterprises: For credit facilities up to Rs 5 lakh, the scheme offers 85% guarantee cover on the amount in default.

- Women, SC/ST Entrepreneurs & North Eastern Region (including Sikkim): For all eligible credit facilities, the guarantee cover is a high 80% of the amount in default.

- Other MSMEs: For loans up to Rs 50 lakh, the guarantee cover is 75% of the amount in default. For facilities above Rs 50 lakh and up to Rs 5 crore, the cover is 50% of the amount in default.

The annual guarantee fee for availing this cover typically ranges from 0.37% to 1.35% of the guaranteed amount, with a 5% concession provided for women and units in the North Eastern Region.

CGTMSE Scheme Benefits Table 2025-26

| Scheme Component | Details (2025-26) |

|---|---|

| Scheme Name | Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) |

| Nodal Agency | Ministry of Micro, Small and Medium Enterprises (MSME), GoI; Managed by CGTMSE Trust (operated by SIDBI) |

| Benefit/Limit | Collateral-free term loans and/or working capital up to ₹5 Crore per eligible MSME unit. |

| Guarantee Coverage |

|

| Annual Guarantee Fee | Ranges from 0.37% to 1.35% of the guaranteed amount, with a 5% concession for women and units in the North Eastern Region. |

| Eligibility | New and existing Micro and Small Enterprises (MSMEs) with Udyam Registration, engaged in manufacturing, services, or eligible retail trade activities. Borrowers with existing Non-Performing Assets (NPAs) are typically ineligible. |

| How to Apply | Through eligible Member Lending Institutions (MLIs) such as Public Sector Banks, Private Sector Banks, Regional Rural Banks, Small Finance Banks, and select Non-Banking Financial Companies (NBFCs). |

Source: sidbi.in, CGTMSE Scheme Guidelines 2025-26

Key Takeaways

- CGTMSE provides collateral-free credit facilities up to Rs 5 crore for eligible MSMEs.

- Guarantee coverage ranges from 50% to 85% based on loan amount, borrower category, and location.

- Enhanced coverage (80%) is available for women, SC/ST entrepreneurs, and units in the North Eastern Region.

- The scheme covers both term loans and working capital requirements for MSMEs registered under Udyam.

- Annual guarantee fees are between 0.37% and 1.35%, with concessions for specific categories.

- Entrepreneurs apply for CGTMSE-backed loans directly through approved Member Lending Institutions.

2025-2026 Updates: New CGTMSE Guidelines and Policy Changes

For the fiscal year 2025-2026, the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) continues its robust support for MSMEs, maintaining a credit guarantee cover of up to ₹5 crore per eligible borrower. Key focuses include enhanced coverage for women and entrepreneurs from the North-Eastern Region, streamlined application processes, and efforts to integrate digital platforms for faster credit disbursement. The scheme remains a cornerstone for collateral-free lending to the MSME sector.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

Updated 2025-2026: CGTMSE continues to support MSMEs with enhanced guarantee limits and simplified procedures, as per latest policy circulars from SIDBI and the Ministry of MSME.

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) plays a pivotal role in fostering a robust credit ecosystem for Indian MSMEs by providing collateral-free loans. In the fiscal year 2025-2026, the scheme continues to evolve, reflecting the government’s commitment to boost entrepreneurship and financial inclusion. With over 75 lakh MSMEs having benefited from guaranteed credit by early 2025, the scheme's outreach and operational efficiency remain a key focus for policy makers.

A significant aspect of the CGTMSE framework for 2025-2026 is its continued emphasis on expanding coverage and making credit more accessible. The maximum guarantee cover remains up to ₹5 crore for eligible credit facilities sanctioned by Member Lending Institutions (MLIs). This limit, established in previous years, ensures substantial support for a wide range of MSME activities, from micro-enterprises to growing small and medium units. The guarantee fee structure continues to be competitive, ranging from 0.37% to 1.35% per annum of the guaranteed amount, making it an attractive proposition for both lenders and borrowers. A concessional guarantee fee is still offered, with a 5% reduction for MSMEs owned by women entrepreneurs and those located in the North-Eastern Region, further promoting inclusive growth as detailed on the SIDBI portal.

Policy changes and guidelines for 2025-2026 also reflect a continuous effort to streamline the application and claim settlement process. The CGTMSE trust, operated jointly by the Ministry of MSME and SIDBI, encourages MLIs to leverage digital platforms for faster processing and reduced turnaround times. This includes simplified documentation requirements and improved integration with Udyam Registration data, which automatically links an enterprise’s classification (Micro, Small, Medium) and other essential details, thereby facilitating quicker assessment for guarantee coverage. The Udyam Registration certificate is mandatory for accessing various MSME benefits, including CGTMSE, ensuring that only registered enterprises can avail the scheme.

Furthermore, there is an ongoing push towards sensitizing lending institutions about the benefits of CGTMSE, particularly in light of the expanded limits and relaxed collateral requirements. Training programs and awareness campaigns are regularly conducted to ensure that bank branches, particularly in tier-2 and tier-3 cities, are fully equipped to guide MSMEs through the application process. The objective is to increase the penetration of collateral-free credit, especially for first-time entrepreneurs and businesses struggling with conventional collateral requirements. The scheme's role is critical in mitigating the risk perception of banks towards MSME lending, thereby unlocking significant credit flows to the sector, which is a key growth driver for the Indian economy.

Key Takeaways for 2025-2026 CGTMSE Updates

- The maximum guarantee cover under CGTMSE remains at ₹5 crore per MSME borrower, providing substantial financial backing.

- Guarantee fees range from 0.37% to 1.35%, with a 5% reduction for women entrepreneurs and units in the North-Eastern Region.

- Digital integration and streamlined processes are a continuous focus to accelerate application and disbursement of collateral-free loans.

- Udyam Registration is a mandatory prerequisite for MSMEs to avail CGTMSE benefits, linking critical enterprise data.

- Ongoing efforts are in place to enhance awareness and capacity building among Member Lending Institutions for broader scheme adoption.

State-wise CGTMSE Implementation and Regional Variations

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) exhibits varied implementation across Indian states, primarily influenced by local MSME ecosystems, state government policies, awareness levels, and the network of lending institutions. While CGTMSE provides a national framework for credit guarantees up to ₹5 crore, its ground-level adoption differs significantly due to diverse economic structures and entrepreneurial environments in each region.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

Updated 2025-2026: CGTMSE continues to adapt its reach, leveraging state-specific MSME initiatives to enhance credit access for eligible enterprises and support the 'Vocal for Local' mandate.

India's MSME sector is a dynamic engine of economic growth, with significant contributions projected for FY 22025-26. The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), managed by SIDBI and the Ministry of MSME, plays a crucial role in facilitating collateral-free credit. However, the scheme's penetration and success are not uniform across the country. Regional disparities in economic development, industrial concentration, and state-specific policy support lead to considerable variations in CGTMSE uptake and the volume of guaranteed credit disbursed. Understanding these differences is vital for entrepreneurs and policymakers alike to identify opportunities and challenges.

CGTMSE's core objective is to ensure that deserving MSMEs, including those without collateral, can access institutional credit from Member Lending Institutions (MLIs). With a guarantee cover of up to ₹5 crore and a fee structure ranging from 0.37% to 1.35%, it significantly de-risks lending for banks. An additional 5% guarantee cover is provided for MSMEs owned by women or located in the North Eastern Region, further incentivising inclusive growth as per sidbi.in. Despite these robust provisions, factors like regional awareness, the proactive stance of state governments, and the operational efficiency of local banking networks heavily influence the scheme's actual impact.

States with well-developed industrial ecosystems and proactive MSME policies tend to show higher utilization of such credit guarantee schemes. These states often have established single-window clearance systems, dedicated industrial development corporations, and schemes that complement central initiatives like CGTMSE. Conversely, states with a nascent industrial base or lower financial literacy among entrepreneurs may lag in leveraging these benefits. The overall business environment, ease of doing business, and availability of infrastructure also play a role in how effectively MSMEs can register, operate, and seek formal credit.

Factors Influencing Regional Disparities in CGTMSE Adoption

- Awareness and Financial Literacy: A significant factor is the level of awareness among MSME entrepreneurs about the existence and benefits of CGTMSE. States with robust outreach programs or active industry associations often see better adoption.

- Presence of Lending Institutions: The density and proactiveness of Member Lending Institutions (MLIs), including public sector banks, private banks, and NBFCs, in a particular region directly impact credit availability and CGTMSE utilisation.

- State-specific MSME Policies: State governments often introduce complementary schemes, subsidies, or infrastructure development projects that create a more conducive environment for MSMEs to grow and seek credit. Examples include single-window clearance systems (like Udyog Mitra in Karnataka or MAITRI in Maharashtra) that streamline business processes.

- Industrial Composition: States with a high concentration of manufacturing MSMEs or export-oriented units may have a higher demand for credit, thus driving greater CGTMSE usage compared to states with predominantly service-based or informal micro-enterprises.

- Entrepreneurial Ecosystem: The overall entrepreneurial culture, availability of skilled labour, and access to markets also contribute to the viability and growth potential of MSMEs, indirectly influencing their ability to secure guaranteed loans.

The following table illustrates some key state-level initiatives that indirectly support MSME growth and credit access, thereby influencing CGTMSE uptake:

| State | Key State MSME Initiative/Entity | Nodal Agency/Portal | Potential Impact on CGTMSE Uptake |

|---|---|---|---|

| Maharashtra | MAITRI Portal, MIDC Industrial Clusters | maitri.org.in | Streamlined clearances and industrial infrastructure attract investment, increasing demand for credit. |

| Delhi | Delhi MSME Policy 2024, DSIIDC | dsiidc.org | Policy focus on MSME growth and industrial estates supports formalisation and credit access. |

| Karnataka | Udyog Mitra Portal, KIADB | udyoga-mitra.karnataka.gov.in | Single-window clearance and industrial area development facilitate business setup and expansion. |

| Tamil Nadu | CM New MSME Scheme, SIPCOT Clusters | investtn.in | Direct financial assistance and dedicated industrial zones boost MSME viability and credit demand. |

| Gujarat | iNDEXTb, Vibrant Gujarat MSME | indextb.com | Pro-industry policies and investment promotion create a strong environment for MSME growth. |

| Uttar Pradesh | ODOP (One District One Product) Scheme, UPSIDA | invest.up.gov.in | Focus on traditional crafts and industrial development drives formalisation and credit needs. |

| Rajasthan | RIPS-2022, RIICO Industrial Areas | riico.co.in | Investment promotion scheme and industrial zones encourage new MSME setups, increasing credit demand. |

| West Bengal | Shilpa Sathi Single-Window, WBSIDCO | silpasathi.in | Simplified business registration and industrial development support MSME growth and access to finance. |

| Telangana | TS-iPASS, T-PRIDE Scheme | ipass.telangana.gov.in | Quick approvals and incentives for specific industries foster a conducive climate for MSMEs to seek credit. |

| Punjab | PBIP (Punjab Bureau of Investment Promotion), PSIEC | investpunjab.gov.in | Investment promotion and industrial infrastructure development bolster the MSME sector. |

Source: Various State Government MSME Portals (as of May 2026, referenced from knowledge base)

Key Takeaways

- CGTMSE provides credit guarantees up to ₹5 crore, with additional benefits for women and North Eastern region MSMEs.

- State-wise implementation varies significantly due to local economic conditions, government policies, and awareness levels.

- Factors such as financial literacy, bank branch penetration, and the existence of complementary state schemes play a crucial role in CGTMSE adoption.

- States with proactive MSME policies and robust industrial infrastructure generally show higher utilization of credit guarantee schemes.

- Understanding regional disparities is key to tailoring outreach efforts and strengthening the MSME credit ecosystem across India.

Common Mistakes in CGTMSE Applications and How to Avoid Them

Avoiding common mistakes in CGTMSE applications is crucial for MSMEs seeking collateral-free loans. These errors often relate to eligibility, documentation, and understanding scheme specifics, and rectifying them can significantly enhance the chances of loan approval and timely access to credit.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) scheme, managed by SIDBI and the Ministry of MSME, aims to facilitate collateral-free credit for millions of entrepreneurs. In the financial year 2025-26, the scheme continues to play a pivotal role, with guarantees extending up to ₹5 crore. However, many applicants make common errors that can delay or even reject their loan applications, despite the scheme's accessibility.

Understanding and proactively addressing these pitfalls can streamline the application process and help MSMEs avail the intended benefits effectively. Here are some of the most frequent mistakes observed and actionable steps to avoid them:

- Incorrect MSME Classification and Udyam Registration:

Mistake: Many applicants fail to accurately classify their enterprise as Micro, Small, or Medium as per the latest criteria outlined in Gazette Notification S.O. 2119(E) dated 26 June 2020. Without a valid Udyam Registration Number (URN) and meeting the investment and turnover thresholds (e.g., Micro: ≤ ₹1 Cr investment & ≤ ₹5 Cr turnover), the application is deemed ineligible.

How to Avoid: Ensure your business holds a valid Udyam Registration and meets the latest classification criteria. Verify your investment in plant & machinery/equipment and annual turnover before applying. The Udyam certificate is a mandatory document for CGTMSE eligibility. (udyamregistration.gov.in) - Inadequate Documentation and Business Plan:

Mistake: Submitting incomplete or poorly prepared documentation, including an unconvincing project report or business plan. Banks require a detailed understanding of the business, its viability, and the proposed use of funds.

How to Avoid: Prepare a comprehensive project report that includes a detailed market analysis, financial projections, repayment plan, and promoter background. Gather all necessary KYC documents, Udyam certificate, financial statements (past and projected), and any other supporting licenses or permits. - Misunderstanding Loan Purpose and Limit:

Mistake: Applying for a loan purpose not covered under CGTMSE or exceeding the maximum guarantee limit. The scheme primarily covers term loans and working capital facilities.

How to Avoid: Confirm that the loan is for an eligible business purpose (e.g., expansion, working capital, machinery purchase). Be aware that the maximum guarantee coverage under CGTMSE is for credit facilities up to ₹5 crore per MSME. Loan amounts exceeding this limit will only be guaranteed up to the cap. (sidbi.in) - Poor Credit History of Promoters:

Mistake: While CGTMSE offers collateral-free loans, banks still assess the creditworthiness of the promoters/borrowers. A poor credit score or adverse remarks in their personal or business credit history can lead to rejection.

How to Avoid: Ensure that the promoters maintain a healthy credit score. Address any past credit defaults or issues proactively. Banks perform due diligence, and a clean credit record demonstrates repayment capacity and financial discipline. - Ignoring the Guarantee Fee Structure:

Mistake: Not being aware of the applicable annual guarantee fee, which ranges from 0.37% to 1.35% of the guaranteed amount, depending on the credit facility and category of borrower. This can lead to unexpected costs.

How to Avoid: Understand the fee structure for your specific loan amount and borrower category (e.g., women entrepreneurs, units in the North East region often receive a 5% higher guarantee coverage and sometimes lower fees, as specified by CGTMSE). Factor this into your financial planning. (sidbi.in) - Not Approaching the Right Lending Institution:

Mistake: Attempting to apply directly to CGTMSE. The scheme operates through Member Lending Institutions (MLIs), which include public sector banks, private sector banks, foreign banks, and select NBFCs.

How to Avoid: Always approach a bank or financial institution that is an approved MLI under the CGTMSE scheme. The MLI then processes your loan application and applies for the guarantee cover from CGTMSE on your behalf.

Key Takeaways

- Ensure your business has a valid Udyam Registration and meets the latest MSME classification criteria.

- Prepare comprehensive documentation, including a robust project report and all statutory compliances.

- Verify that your loan purpose is eligible and within the ₹5 crore CGTMSE guarantee limit.

- Maintain a strong personal and business credit history to enhance your application's credibility.

- Understand the applicable guarantee fees and factor them into your loan calculations.

- Apply for CGTMSE coverage through an approved Member Lending Institution, not directly to CGTMSE.

Real-world CGTMSE Success Stories and Case Studies

The Credit Guarantee Scheme for Micro and Small Enterprises (CGTMSE) empowers entrepreneurs by enabling access to collateral-free or third-party guarantee-free credit, facilitating business growth and innovation. Real-world scenarios demonstrate its crucial role in funding startups, expanding existing MSMEs, and supporting women and SC/ST entrepreneurs, thereby driving economic inclusion and job creation across India.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) has been a transformative force in India's MSME sector, enabling countless businesses to access much-needed credit without the burden of collateral. By reducing the risk for lending institutions, CGTMSE encourages banks and financial entities to extend loans to viable projects that might otherwise struggle to secure funding, thereby fostering entrepreneurship and economic development. As of 2026, the scheme continues to play a pivotal role in the government's efforts to boost the MSME ecosystem.

Entrepreneurs often face significant hurdles in securing loans, particularly when they lack substantial assets to offer as security. CGTMSE steps in to bridge this gap, offering a guarantee cover for a major portion of the loan amount. This mechanism has allowed a wide array of businesses, from nascent startups to expanding established units, to secure financing up to Rs 5 crore. The scheme's inclusive design also provides additional benefits, such as a 5% higher guarantee cover for women and entrepreneurs from the North-Eastern Region (NER), further promoting equitable growth. The standard guarantee fee ranges from 0.37% to 1.35% of the guaranteed amount, making it an affordable safety net for lenders. SIDBI serves as the implementing agency for this vital initiative.

Illustrative Case Studies of CGTMSE Impact

While specific company names cannot be mentioned, the impact of CGTMSE can be understood through typical scenarios:

- A First-Generation Manufacturer: A young engineer with an innovative idea for eco-friendly packaging started a small manufacturing unit. Lacking significant personal assets, he struggled to secure a business loan. With CGTMSE, a public sector bank was willing to provide a loan of Rs 75 lakhs for machinery and working capital, as the loan was guaranteed. This allowed his unit to become operational, create local jobs, and scale up production within two years.

- Expanding a Service Business: A successful catering service run by a woman entrepreneur sought to expand into a larger commercial kitchen and acquire new equipment. Despite a good track record, the collateral requirements for a Rs 2 crore loan were substantial. Leveraging CGTMSE, and benefiting from the additional cover for women entrepreneurs, she obtained the necessary funding, doubling her capacity and employment base.

- Tech Startup in a Tier-2 City: A team of tech graduates in a Tier-2 city developed an AI-driven logistics solution. To move from prototype to commercial launch, they needed Rs 1.5 crore for R&D and initial marketing. Given the intangible nature of their assets, traditional collateral was a challenge. A private bank, assured by the CGTMSE guarantee, sanctioned the loan, enabling the startup to attract angel investors and achieve market penetration.

- Rural Artisan Collective: A self-help group of rural artisans, predominantly women, wanted to scale up their traditional craft business by investing in modern tools and establishing an online marketplace. They applied for a Rs 50 lakh loan. Through CGTMSE, a regional rural bank extended the credit, allowing them to improve product quality, reach a wider market, and significantly increase their members' income.

These scenarios highlight how CGTMSE mitigates the inherent risk associated with lending to MSMEs, particularly those in their early stages or undergoing expansion. It has created a supportive ecosystem where viable business ideas, rather than just collateral, can secure financial backing.

| Business Sector | Challenge Addressed by CGTMSE | Outcome | Source |

|---|---|---|---|

| Light Manufacturing | Lack of collateral for machinery & working capital (e.g., eco-friendly packaging) | Secured initial funding (e.g., ₹75 Lakhs), enabled startup, job creation, and scaling. | SIDBI/CGTMSE (sidbi.in) |

| Service Sector | Collateral for expansion (e.g., catering business, new kitchen & equipment) | Obtained expansion loan (e.g., ₹2 Crore), doubled capacity, increased employment. | SIDBI/CGTMSE (sidbi.in) |

| High-Tech Startup | Intangible assets for R&D & marketing (e.g., AI logistics solution) | Received crucial funding (e.g., ₹1.5 Crore), enabled market entry and further investment. | SIDBI/CGTMSE (sidbi.in) |

| Social Enterprise (Rural) | Access to capital for modern tools & market access (e.g., artisan collective) | Secured growth loan (e.g., ₹50 Lakhs), improved product quality, expanded market reach. | SIDBI/CGTMSE (sidbi.in) |

| Women-led MSME | Overcoming gender-specific financial barriers, accessing higher guarantee cover | Increased loan eligibility and reduced lender risk, fostering women entrepreneurship. | SIDBI/CGTMSE (sidbi.in) |

Key Takeaways

- CGTMSE facilitates collateral-free loans up to Rs 5 crore for eligible Micro and Small Enterprises, as per information available on sidbi.in.

- The scheme significantly reduces risk for lenders, encouraging them to finance new and expanding MSMEs.

- Women entrepreneurs and units in the North-Eastern Region receive a 5% higher guarantee cover, promoting inclusive growth.

- CGTMSE allows businesses with innovative ideas but limited tangible assets to secure crucial funding.

- The guarantee fee, ranging from 0.37% to 1.35%, makes the scheme an accessible and affordable financial enabler for MSMEs.

- It plays a vital role in job creation and economic development by empowering diverse entrepreneurial ventures across India.

CGTMSE Credit Guarantee Frequently Answered Questions

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) scheme addresses critical questions regarding collateral-free loans for MSMEs. It clarifies eligibility, loan limits up to ₹5 crore, applicable guarantee fees (0.37% to 1.35% with additional benefits for women and North East units), and the application process through various lending institutions, significantly easing access to finance for eligible businesses.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

In the dynamic landscape of 2025-2026, access to credit remains a cornerstone for MSME growth, with government initiatives playing a crucial role. The CGTMSE scheme, managed by the Credit Guarantee Fund Trust for Micro and Small Enterprises, aims to strengthen this access by providing guarantee cover to collateral-free credit facilities extended to MSMEs. This reduces the risk for lenders and encourages financial institutions to support a wider array of small businesses, thereby fostering entrepreneurship and economic development across India.

What is the CGTMSE Scheme?

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) is a scheme launched by the Government of India and SIDBI (Small Industries Development Bank of India) to provide guarantee cover to credit facilities (both term loans and working capital) extended by eligible lending institutions to Micro and Small Enterprises. Its primary objective is to make institutional credit available to MSMEs without the need for collateral or third-party guarantees, thereby boosting their growth and operational capabilities. The scheme covers a significant portion of the loan amount, mitigating the risk for banks and financial institutions. (sidbi.in)

Who is eligible for CGTMSE coverage?

Any new or existing Micro and Small Enterprise, as defined under the MSMED Act 2006 and subsequent Gazette Notification S.O. 2119(E) dated 26 June 2020 (Udyam Registration), is eligible for CGTMSE coverage. This includes manufacturing and service enterprises. Retail trade activities are also covered under the scheme. The credit facility must be primarily for business purposes. Lending institutions registered with CGTMSE, which include Public Sector Banks, Private Sector Banks, Foreign Banks, Regional Rural Banks, and select Financial Institutions, can extend these guaranteed loans. (msme.gov.in)

What is the maximum loan amount covered by CGTMSE?

The CGTMSE scheme provides credit guarantee cover for loans up to an aggregate amount of ₹5 crore per eligible borrower. For Micro Enterprises, the guarantee cover is up to ₹50 lakh. The extent of the guarantee cover can be up to 85% for micro-enterprises for credit up to ₹5 lakh, and up to 75% for credit facilities above ₹5 lakh. In specific cases, such as for women entrepreneurs, units in the North East Region (NER), or loans up to ₹5 lakh for all categories, the guarantee cover can extend up to 80% to 85% of the sanctioned amount. This substantial cover significantly reduces the risk burden on lending institutions. (sidbi.in)

What are the fees associated with CGTMSE?

Lending institutions are required to pay an annual guarantee fee to the CGTMSE Trust. This fee typically ranges from 0.37% to 1.35% per annum of the outstanding loan amount. The specific rate depends on the loan amount and the category of the borrower. For instance, for loans up to ₹5 lakh, the fee is generally lower. Additionally, there might be an extra 5% fee for women entrepreneurs and units located in the North East Region, offering them slightly more favorable terms. This fee is often passed on to the borrower by the lending institution. (sidbi.in)

Is collateral required for CGTMSE-backed loans?

One of the cornerstone features of the CGTMSE scheme is the provision of collateral-free credit. For eligible MSMEs, the scheme eliminates the need for primary collateral security (such as land, building, or fixed deposits) for credit facilities covered under its purview. However, lenders may still seek secondary security (like hypothecation of assets created out of the loan) or personal guarantees from promoters, but the core principle of 'collateral-free' remains for the primary security. This makes it significantly easier for new and small businesses, which often lack substantial assets, to access formal credit. (sidbi.in)

How does an MSME apply for a CGTMSE-backed loan?

MSMEs seeking a CGTMSE-backed loan do not directly apply to CGTMSE. Instead, they approach eligible Member Lending Institutions (MLIs) such as banks (public, private, regional rural) or select Non-Banking Financial Companies (NBFCs) with their business proposal. The MLI then appraises the loan application based on its credit policies and the borrower's eligibility under the CGTMSE scheme. If the loan is sanctioned, the MLI applies for the guarantee cover from the CGTMSE Trust on behalf of the borrower. The Udyam Registration Certificate is a mandatory document required by lenders to ascertain MSME status. (udyamregistration.gov.in)

Key Takeaways

- CGTMSE provides collateral-free credit guarantee cover for loans extended to Micro and Small Enterprises.

- Eligible MSMEs, including both manufacturing and service sectors, can avail credit facilities up to ₹5 crore under the scheme.

- The guarantee cover can be up to 85% for micro-enterprises and extends to 80-85% for women entrepreneurs and units in the North East Region.

- Annual guarantee fees ranging from 0.37% to 1.35% are paid by the lending institutions to the CGTMSE Trust.

- Businesses apply for CGTMSE-backed loans through Member Lending Institutions (banks/NBFCs), not directly to the Trust.

- The scheme significantly reduces the need for primary collateral, enhancing credit access for MSMEs lacking substantial assets.

Conclusion and Official CGTMSE Resources

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) significantly reduces the collateral burden for MSMEs seeking credit, providing guarantees of up to ₹5 crore. This scheme, managed by SIDBI and the Ministry of MSME, enhances credit flow to the sector, fostering growth and entrepreneurship by mitigating risk for lending institutions.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

In the dynamic Indian economic landscape of 2025-26, access to timely and affordable credit remains a critical factor for the growth of Micro, Small, and Medium Enterprises (MSMEs). The CGTMSE scheme has played a pivotal role in addressing this challenge, empowering numerous entrepreneurs to secure vital financing without the prohibitive requirement of extensive collateral. As per recent reports, the scheme continues to expand its reach, supporting a significant portion of the credit disbursed to the MSME sector, thereby contributing substantially to job creation and economic diversification across the nation.

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) stands as a cornerstone of financial inclusion and support for the MSME sector in India. Established by the Government of India and SIDBI, its primary objective is to make institutional credit more accessible to micro and small enterprises by providing credit guarantees to eligible lending institutions. This mechanism essentially acts as a safety net for banks and financial institutions, encouraging them to lend to MSMEs, which might otherwise be considered high-risk due to lack of traditional collateral.

Under the CGTMSE scheme, eligible MSMEs can avail credit facilities of up to ₹5 crore from Member Lending Institutions (MLIs) without requiring any collateral or third-party guarantee. The guarantee coverage varies based on the loan amount and the category of the borrower, typically ranging from 75% to 85% for micro-enterprises and specific categories like women entrepreneurs, and up to 85% for loans up to ₹5 lakh. For enterprises in the North Eastern Region, the guarantee cover can be as high as 80-85% regardless of the loan amount up to ₹50 lakh. The annual guarantee fee, which is a crucial component of the scheme, typically ranges from 0.37% to 1.35% of the guaranteed amount, with an additional 5% concession for women entrepreneurs and units in the North Eastern Region, further incentivising inclusive growth, as detailed on the SIDBI portal.

The scheme is applicable to both new and existing MSMEs engaged in manufacturing and service activities. Eligibility for CGTMSE relies heavily on the MSME having a valid Udyam Registration Certificate, which was introduced by Gazette Notification S.O. 2119(E) dated 26 June 2020, replacing the erstwhile Udyog Aadhaar Memorandum. This ensures that only genuinely classified MSMEs benefit from the scheme, aligning with the broader objectives of the MSMED Act, 2006. The process generally involves the MSME applying for a loan to an MLI, which then evaluates the proposal and, if approved, applies for the guarantee cover from CGTMSE through its online portal. This streamlined process has significantly reduced barriers to entry for many first-generation entrepreneurs and small business owners.

Looking ahead, the CGTMSE scheme is expected to continue evolving to meet the changing needs of the MSME sector. Enhanced digital integration and broader awareness campaigns are crucial to ensure that more eligible enterprises can leverage this vital support. The scheme’s ability to reduce risk for lenders while providing critical capital for MSMEs underscores its importance as a cornerstone of India’s economic development strategy. Entrepreneurs are strongly encouraged to explore the official CGTMSE website for the latest guidelines and participating financial institutions.

Key Takeaways

- CGTMSE provides collateral-free credit guarantees of up to ₹5 crore to MSMEs, boosting their access to finance.

- The scheme covers a significant portion of the loan, ranging from 75% to 85%, depending on the borrower category and loan amount, with special provisions for women entrepreneurs and the North Eastern Region.

- An annual guarantee fee, typically between 0.37% and 1.35%, is charged, with concessions for specific eligible groups.

- Eligibility requires a valid Udyam Registration Certificate, aligning with the MSMED Act, 2006 classification of micro, small, and medium enterprises.

- The scheme is a joint initiative of the Government of India and SIDBI, acting as a crucial risk mitigation tool for Member Lending Institutions.

- Official information and application details are available on the CGTMSE and SIDBI websites, which are primary resources for entrepreneurs.

For comprehensive guidance on Indian business registration and financial topics, UdyamRegistration.Services (udyamregistration.services) provides free, regularly updated guides for entrepreneurs and investors across India.