Business Loan Without Security: Collateral-Free Options for Indian SMEs

Introduction: The Rise of Collateral-Free Business Financing in India

Collateral-free business financing has emerged as a transformative solution for Indian Micro, Small, and Medium Enterprises (MSMEs), addressing a critical barrier to growth by removing the need for physical assets as security. Driven by government initiatives like the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) and the Pradhan Mantri MUDRA Yojana, these loans facilitate easier access to credit, fostering entrepreneurship and economic development across various sectors. This shift enables a wider range of businesses, particularly startups and those lacking substantial assets, to secure necessary capital for expansion and operational needs.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

In 2026, the Indian economy continues to rely heavily on its vibrant Micro, Small, and Medium Enterprises (MSMEs), which contribute significantly to the nation's GDP and employment. Historically, a major impediment for these businesses, especially startups and those in their nascent stages, has been the inability to provide collateral for business loans. Recognizing this critical gap, the Indian government and financial institutions have progressively introduced and strengthened mechanisms for collateral-free business financing, marking a pivotal shift in the lending landscape.

The journey towards accessible, collateral-free credit for MSMEs gained substantial momentum with the enactment of the Micro, Small and Medium Enterprises Development (MSMED) Act, 2006, which laid the legal framework for recognizing and nurturing these enterprises. However, the real game-changer came with the establishment of schemes designed to mitigate the risk for lenders. The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), managed by SIDBI and the Ministry of MSME, stands out as a flagship initiative. Under this scheme, financial institutions receive a guarantee cover from the trust for loans extended to MSMEs without collateral, covering up to 85% of the defaulted amount, with a maximum guarantee cover of ₹5 crore per eligible unit as per recent updates. This mechanism significantly reduces the perceived risk for banks and Non-Banking Financial Companies (NBFCs), encouraging them to lend more freely to the sector. The guarantee fee typically ranges from 0.37% to 1.35% per annum, with additional concessions for women entrepreneurs and units in the North-Eastern Region, fostering inclusive growth sidbi.in.

Further expanding the reach of collateral-free financing, the Pradhan Mantri MUDRA Yojana (PMMY), launched in 2015, specifically targets micro-enterprises and individuals looking to start or expand small businesses. It offers loans up to ₹10 lakh without requiring collateral, categorized into Shishu (up to ₹50,000), Kishore (₹50,001 to ₹5 lakh), and Tarun (₹5 lakh to ₹10 lakh) mudra.org.in. This scheme has been instrumental in supporting a vast number of small-scale entrepreneurs, including street vendors, small shopkeepers, and service sector providers, by addressing their immediate capital needs. The success of MUDRA can be seen in the sheer volume of loans disbursed, empowering millions to pursue their entrepreneurial aspirations without the burden of pledging assets.

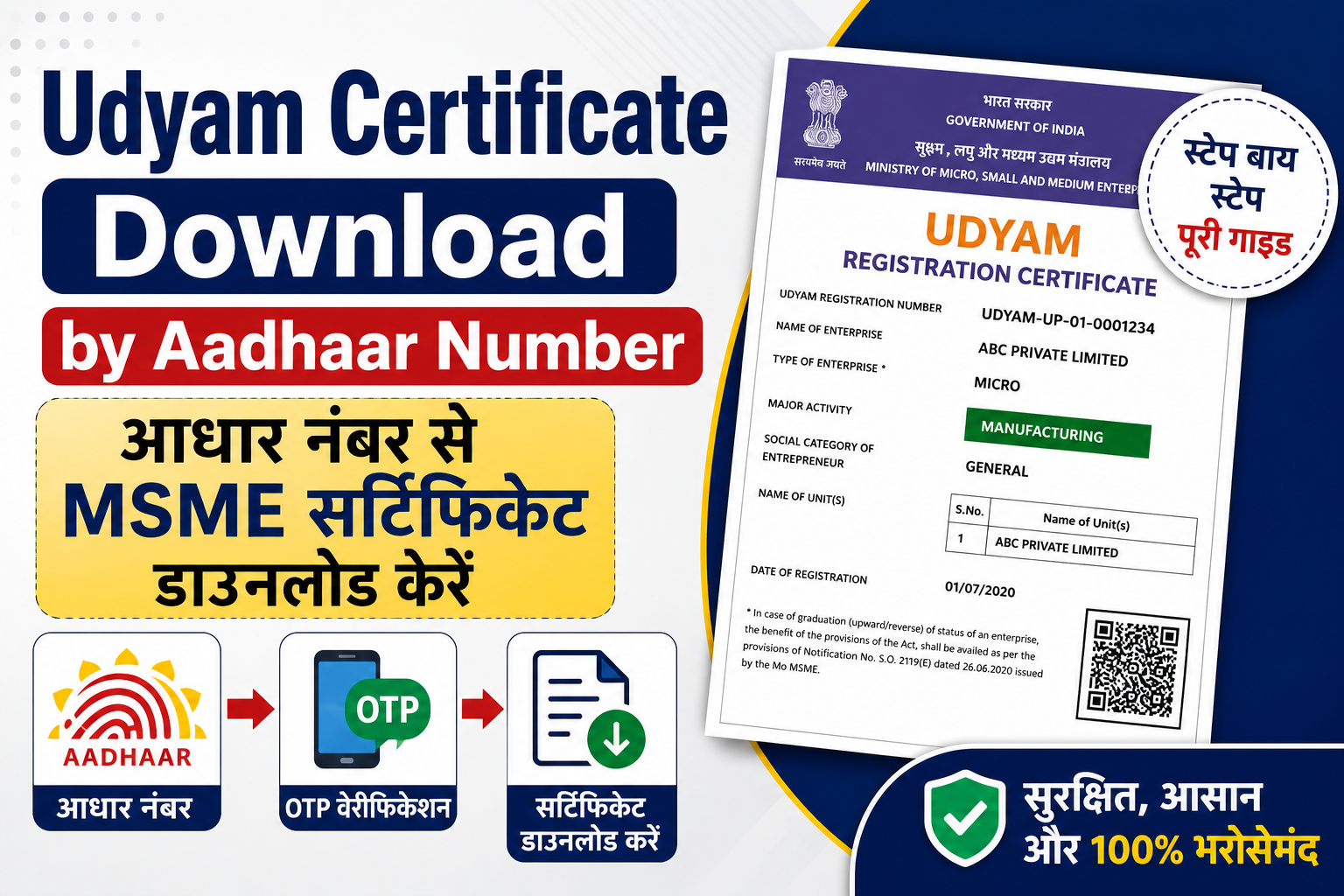

The importance of Udyam Registration also cannot be overstated in this ecosystem. Introduced via Gazette Notification S.O. 2119(E) dated 26 June 2020, replacing the earlier Udyog Aadhaar Memorandum, Udyam Registration simplifies the process for MSMEs to obtain official recognition. An Udyam Certificate serves as a crucial document for businesses to avail themselves of the various benefits offered under the MSMED Act 2006, including priority sector lending, interest rate subsidies, and access to collateral-free loan schemes like CGTMSE. The registration process is entirely free and online, requiring only a Permanent Account Number (PAN) and Goods and Services Tax Identification Number (GSTIN), and for informal micro units, the Udyam Assist Platform launched in January 2023 provides an alternative registration route udyamregistration.gov.in.

The convergence of robust government schemes, simplified registration processes, and a growing financial sector willingness has democratized access to credit. This paradigm shift from traditional asset-backed lending to a more trust and viability-based model is crucial for India's economic resilience, especially as the nation aims for ambitious growth targets in the coming years. Collateral-free financing not only fuels immediate business needs but also encourages innovation and risk-taking among entrepreneurs who might otherwise be constrained by a lack of tangible assets.

Key Takeaways

- Collateral-free loans address a primary hurdle for Indian MSMEs, enabling broader access to credit for businesses lacking physical assets.

- The CGTMSE scheme provides guarantee cover up to ₹5 crore (85% of defaulted amount) to lenders for collateral-free loans, reducing their risk exposure sidbi.in.

- Pradhan Mantri MUDRA Yojana offers collateral-free loans up to ₹10 lakh for micro-enterprises, categorized as Shishu, Kishore, and Tarun, specifically aiding small-scale entrepreneurs mudra.org.in.

- Udyam Registration, as per Gazette S.O. 2119(E) dated 26 June 2020, is crucial for MSMEs to avail themselves of these benefits, being a free, online process udyamregistration.gov.in.

- These initiatives collectively foster entrepreneurship, economic growth, and financial inclusion by shifting the lending paradigm towards trust and business viability.

What is a Business Loan Without Security? Understanding Unsecured Lending

A business loan without security, also known as an unsecured business loan, is a type of financing where the borrower is not required to pledge any collateral or assets to the lender. Lenders assess eligibility primarily based on the business's creditworthiness, financial health, turnover, and repayment capacity, making it an accessible option for Micro, Small, and Medium Enterprises (MSMEs) in India that may lack tangible assets for collateral.

In India's dynamic economic landscape, access to finance is crucial for the growth of MSMEs, which contribute significantly to employment and GDP. For many emerging businesses and startups, pledging assets as collateral can be a significant hurdle to securing funding. Recognizing this, the market for business loans without security has expanded, offering a lifeline to entrepreneurs seeking capital without encumbering their personal or business assets.

An unsecured business loan fundamentally differs from a secured loan in one critical aspect: the absence of collateral. While secured loans require assets such as property, machinery, or inventory to be pledged, unsecured loans rely solely on the borrower's creditworthiness and perceived ability to repay. This credit assessment typically involves a thorough review of the business's financial statements, tax filings, bank transaction history, and the promoter's credit score. The lender assumes a higher risk in unsecured lending, which is often reflected in higher interest rates compared to secured counterparts.

Key Characteristics of Unsecured Business Loans:

- No Collateral Requirement: This is the defining feature. Businesses, especially startups and those in the service sector, often find this appealing as they may not possess substantial fixed assets to offer as security.

- Faster Processing: The absence of asset valuation and legal documentation for collateral can significantly expedite the loan application and disbursement process, a critical advantage for businesses requiring quick access to funds.

- Higher Interest Rates: Due to the increased risk borne by lenders, unsecured loans generally carry higher interest rates. The specific rate depends on the lender's risk assessment, the borrower's credit profile, and market conditions.

- Stricter Eligibility Criteria: Lenders typically impose rigorous eligibility requirements, focusing on the business's vintage, annual turnover, profitability, and the promoter's CIBIL score. A strong repayment history and consistent cash flow are paramount.

- Smaller Loan Amounts: While not universally true, unsecured loans often have a lower maximum limit compared to secured loans, reflecting the lender's mitigated risk exposure.

Several government-backed schemes and private financial institutions in India offer unsecured business loans. A notable example is the Pradhan Mantri MUDRA Yojana (PMMY), launched under the Micro Units Development and Refinance Agency (MUDRA) Bank. This scheme provides collateral-free loans up to ₹10 lakhs to micro and small enterprises in manufacturing, trading, and services. The loans are categorized into Shishu (up to ₹50,000), Kishore (₹50,001 to ₹5 lakhs), and Tarun (₹5 lakhs to ₹10 lakhs), facilitated through commercial banks, RRBs, SFBs, and NBFCs, as detailed on mudra.org.in.

Furthermore, many Non-Banking Financial Companies (NBFCs) and FinTech platforms specialize in offering unsecured business loans by leveraging advanced data analytics to assess credit risk, often providing more flexible repayment options and faster approvals than traditional banks. For financial year 2025-26, the demand for such flexible, collateral-free financing options among Indian SMEs is projected to remain high as businesses seek to expand operations, manage working capital, and invest in technology without asset encumbrance.

Key Takeaways

- Unsecured business loans do not require collateral, making them ideal for MSMEs lacking substantial assets.

- Lenders assess eligibility based on a business's creditworthiness, turnover, financial health, and the proprietor's credit score.

- These loans generally offer faster processing but come with higher interest rates due to increased lender risk.

- The Pradhan Mantri MUDRA Yojana (PMMY) is a significant government initiative providing collateral-free loans up to ₹10 lakhs to micro and small enterprises.

- Other lenders, including NBFCs and FinTechs, also offer unsecured options, often with streamlined application processes.

Who is Eligible for Unsecured Business Loans in India

Eligibility for unsecured business loans in India depends on various factors including business type, operational history, financial health, and credit score. While private lenders assess criteria like annual turnover and CIBIL score, government schemes like PMMY and CGTMSE focus on specific enterprise categories, primarily Micro, Small, and Medium Enterprises (MSMEs) with Udyam Registration, supporting both new and existing businesses.

In the dynamic Indian business landscape of 2025-26, access to finance without collateral is crucial for the growth of small and medium enterprises. A significant portion of India's 6.3 crore MSMEs, as per recent government reports, often seek such funding. Lenders, both traditional banks and NBFCs, and government-backed schemes, evaluate a range of criteria to determine a business's eligibility for unsecured loans, focusing on its ability to repay rather than asset pledges.

Understanding who qualifies for these loans involves looking at both general requirements set by private financial institutions and the specific mandates of government initiatives designed to foster entrepreneurship and economic development.

Key Factors Lenders Consider for Unsecured Loans

Private lenders, including banks and Non-Banking Financial Companies (NBFCs), assess several critical parameters before approving unsecured business loans:

- Business Type and Registration: Loans are typically extended to Sole Proprietorships, Partnership Firms, Limited Liability Partnerships (LLPs), and Private Limited Companies. Proper registration and compliance with regulatory bodies like MCA (for companies/LLPs) are essential.

- Business Vintage: Most lenders require the business to have been operational for a minimum period, usually 1 to 3 years, to demonstrate stability and a consistent track record.

- Annual Turnover: A minimum annual turnover is often mandated, which can range from ₹10 lakh to ₹20 lakh or more, depending on the lender and loan amount. This reflects the business's revenue generation capacity.

- Credit Score: The CIBIL score of the business owner or the entity itself is a crucial determinant. A good credit score, typically 700 or above, indicates responsible financial behavior and significantly enhances eligibility.

- Financial Health and Profitability: Lenders scrutinize audited financial statements, profit & loss accounts, and balance sheets for the last 1-2 years to assess profitability, cash flow, and debt-to-equity ratios. Consistent ITR filings are also reviewed.

- Bank Statements: Six to twelve months of bank statements are usually required to verify transactional history, average monthly balance, and any loan defaults or bounced cheques.

Government-Backed Unsecured Business Loan Schemes

For MSMEs, government schemes play a vital role in providing collateral-free credit. Eligibility for these schemes often centers around the Udyam Registration certificate, which classifies a business as Micro, Small, or Medium as per Gazette Notification S.O. 2119(E) dated 26 June 2020.

- Pradhan Mantri MUDRA Yojana (PMMY): This scheme, administered by Mudra Ltd., offers loans up to ₹10 lakh to non-corporate, non-farm small/micro enterprises. Eligibility is broad, focusing on business viability and a sound business plan. It categorizes loans into Shishu (up to ₹50,000), Kishore (₹50,001 to ₹5 lakh), and Tarun (₹5 lakh to ₹10 lakh).

- Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE): Managed by SIDBI, CGTMSE provides credit guarantees to member lending institutions for collateral-free loans up to ₹5 crore. Eligibility typically requires the MSME to be engaged in manufacturing or service activities, with Udyam registration being a key prerequisite for most banks to process the guarantee.

- Prime Minister's Employment Generation Programme (PMEGP): Operated by KVIC, PMEGP supports new micro-enterprises with a subsidy. For manufacturing units, the maximum project cost is ₹25 lakh, and for service units, it's ₹10 lakh. Eligibility includes individuals aged 18 and above, with a minimum 8th pass qualification for projects above certain limits.

The following table provides a comparative overview of eligibility criteria across different unsecured loan options:

| Eligibility Aspect | General Unsecured Business Loan (Private Lenders) | PMMY (MUDRA Yojana) | CGTMSE Scheme |

|---|---|---|---|

| Business Type | Proprietorship, Partnership, LLP, Pvt Ltd Co. | Non-corporate, non-farm small/micro enterprises | Micro & Small Enterprises (Manufacturing/Service) |

| Business Vintage | Min. 1-3 years operation | New or existing businesses | New or existing MSMEs |

| Minimum Turnover | ₹10-20 Lakhs p.a. (varies by lender) | No strict minimum; assessed on business plan | No strict minimum; assessed by lender |

| Promoter/Business CIBIL Score | Good (typically 700+) | Reasonable credit history preferred | Assessed by Member Lending Institution |

| Udyam Registration | Recommended, but not always mandatory | Not mandatory for direct MUDRA loans, but beneficial for some lenders | Mandatory for most banks to avail guarantee for MSMEs |

| Loan Amount Limit | Up to ₹75 Lakhs - ₹1 Crore (varies) | Up to ₹10 Lakhs (Shishu, Kishore, Tarun) | Up to ₹5 Crore (guarantee cover) |

| Purpose of Loan | Working capital, expansion, equipment purchase | Working capital, capital expenditure, business expansion | Working capital, term loans for business setup/expansion |

Source: MSME Ministry, Mudra, SIDBI, KVIC websites, 2026

Key Takeaways

- Unsecured business loans are available from private lenders and government schemes, each with distinct eligibility criteria.

- General eligibility factors for private lenders include business vintage (1-3 years), annual turnover (₹10-20 lakh+), and a strong CIBIL score (700+).

- Government schemes like PMMY (up to ₹10 lakh) and CGTMSE (up to ₹5 crore guarantee) primarily target Micro and Small Enterprises.

- Udyam Registration is a crucial prerequisite for MSMEs to access benefits under schemes like CGTMSE and often provides an advantage with private lenders.

- The ultimate eligibility is determined by a holistic assessment of a business's financial health, operational history, and compliance with specific scheme guidelines.

Step-by-Step Process to Apply for Collateral-Free Business Loans

Applying for collateral-free business loans in India primarily involves obtaining an Udyam Registration, preparing a robust business plan, and approaching financial institutions offering government-backed schemes like CGTMSE or MUDRA. Thorough documentation and a clear repayment strategy are crucial for successful application and disbursal.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

In 2025-26, MSMEs continue to be the backbone of the Indian economy, with significant government emphasis on improving their access to credit. Collateral-free business loans, largely facilitated by schemes like the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) and Pradhan Mantri MUDRA Yojana, empower millions of entrepreneurs by removing the primary hurdle of asset-based security. Navigating the application process systematically can significantly increase the chances of securing vital funding.

Detailed Application Process for Collateral-Free Loans

- Understand Eligibility and Choose the Right Scheme: Before applying, thoroughly research the various government schemes designed for collateral-free funding. Key options include the Pradhan Mantri MUDRA Yojana (PMMY), offering loans up to Rs 10 lakh in three categories (Shishu, Kishore, Tarun) for micro-enterprises, and the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), which provides credit guarantees to financial institutions for loans up to Rs 5 crore for eligible MSMEs. For manufacturing units or service enterprises, the Prime Minister's Employment Generation Programme (PMEGP) offers substantial subsidies on project costs. Review the specific criteria for each scheme on their respective official portals like mudra.org.in or sidbi.in.

- Obtain Udyam Registration: For most government-backed MSME schemes and their benefits, Udyam Registration is a mandatory prerequisite. This free, online registration process categorizes enterprises as Micro, Small, or Medium based on their investment in plant & machinery/equipment and turnover, as per Gazette Notification S.O. 2119(E) dated 26 June 2020. Your Udyam certificate, obtainable from udyamregistration.gov.in, serves as crucial proof of your MSME status and is automatically synced with ITR and GSTIN data.

- Develop a Comprehensive Business Plan: A well-articulated business plan is critical, especially for loans without collateral. It should detail your business model, market analysis, operational strategy, management team, and most importantly, robust financial projections including sales forecasts, cash flow statements, and a clear repayment schedule. Lenders rely on this document to assess the viability and potential profitability of your venture, which is their primary security in the absence of physical collateral.

- Gather Required Documentation: Prepare all necessary documents meticulously. This typically includes your Udyam Registration Certificate, PAN card, Aadhaar card, business registration documents (e.g., Shop & Establishment Certificate, GSTIN if applicable), bank statements (past 6-12 months), Income Tax Returns (ITRs) for the last 2-3 years, a detailed project report (especially for PMEGP and larger CGTMSE loans), address proof for business and personal residences, and photographs.

- Approach Financial Institutions: Once your documentation and business plan are ready, approach banks (Public Sector, Private Sector), Non-Banking Financial Companies (NBFCs), or Microfinance Institutions (MFIs) that offer the chosen collateral-free loan schemes. Many banks have dedicated MSME loan departments. Enquire about the specific requirements, interest rates, and processing fees for schemes like MUDRA or CGTMSE at your preferred lender.

- Submit Application and Undergo Due Diligence: Complete the loan application form accurately, either online or physically, and submit all required documents. The lender will then conduct a thorough due diligence process, which involves verifying your documents, assessing your creditworthiness (though CIBIL score might be less critical for schemes like MUDRA), and evaluating the business plan's feasibility. Be prepared to answer questions and provide clarifications during this stage.

- Loan Sanction and Disbursal: Upon successful evaluation, the bank will issue a sanction letter detailing the loan amount, interest rate, tenure, and other terms. After you accept the terms and complete any final formalities, the loan amount will be disbursed to your business bank account. Ensure you adhere to the repayment schedule to maintain a good credit history.

Key Takeaways for Collateral-Free Loan Application

- Udyam Registration is a foundational requirement for accessing most MSME-specific collateral-free loan schemes, offering lifetime validity and no renewal.

- Government-backed schemes like CGTMSE provide credit guarantees for loans up to Rs 5 crore, reducing lender risk and making collateral-free options accessible for Small and Medium Enterprises.

- The Pradhan Mantri MUDRA Yojana (PMMY) specifically targets micro-enterprises, offering loans up to Rs 10 lakh in its various categories.

- A detailed and realistic business plan is paramount, serving as the primary assessment tool for lenders when physical collateral is absent.

- Meticulous documentation, including Udyam Certificate, ITRs, and bank statements, streamlines the application process and improves approval chances.

Required Documents and Prerequisites for Unsecured Business Loans

For unsecured business loans, lenders in India primarily assess the borrower's financial health, creditworthiness, and business stability. Key prerequisites include a strong credit score, a proven business vintage, and robust documentation like Udyam Registration, GSTIN, bank statements, and income tax returns to ascertain repayment capacity in the absence of physical collateral.

In the 2025-26 financial landscape, unsecured business loans have become a crucial lifeline for numerous Indian SMEs aiming for expansion without pledging assets. Despite the absence of collateral, financial institutions employ rigorous due diligence, making the submission of accurate and comprehensive documentation paramount. Lenders meticulously evaluate a business's operational history and financial discipline to mitigate risk.

Understanding the specific documents and meeting the prerequisites can significantly streamline the application process. While requirements may vary slightly between lenders, a core set of documents is almost universally requested. This includes proof of business registration, financial statements reflecting consistent performance, and identity verification for the business owners. For MSMEs, possessing a valid Udyam Registration certificate often provides an added advantage, as it qualifies businesses for various government-backed schemes like CGTMSE, which offer credit guarantees for collateral-free loans up to Rs 5 crore (as per sidbi.in).

Furthermore, the timely filing of Income Tax Returns (ITR) and Goods and Services Tax Identification Numbers (GSTIN) data are critical. These provide transparent insights into the business's turnover and profitability, which are direct indicators of repayment capability. For businesses dealing with vendors, compliance with Section 43B(h) of the Income Tax Act, effective AY 2024-25, which mandates payment to MSMEs within 45 days for tax deductibility, can also reflect positively on a business's financial management practices.

Key Prerequisites for Unsecured Business Loans

- Strong Credit Score: A CIBIL score of 700+ for both the business (if applicable) and its promoters/directors is generally preferred, indicating a responsible credit history.

- Business Vintage: Most lenders require the business to be operational for at least 1-3 years to establish a track record of stability.

- Consistent Turnover: Demonstrated regular revenue through bank statements and GST filings is essential.

- Profitability: Evidence of consistent profits, as reflected in audited financial statements or ITRs, assures lenders of repayment capacity.

- Udyam Registration: While not always mandatory, it is highly recommended, especially for availing benefits under schemes like MUDRA or CGTMSE, and signals formal recognition as an MSME (refer udyamregistration.gov.in).

The table below outlines the typical documents required for an unsecured business loan application in India:

| Category | Required Documents | Purpose |

|---|---|---|

| Business Registration & Identity | Udyam Registration Certificate GST Registration Certificate & GSTIN PAN Card (Business Entity & Promoters) Partnership Deed / LLP Agreement / Certificate of Incorporation (as applicable) Business Address Proof (Utility Bill, Rent Agreement) | Confirms legal existence and status of the business and its proprietors. |

| Financial Statements | Bank Statements (Last 6-12 months) Income Tax Returns (Last 2-3 years) with Balance Sheet & Profit & Loss Statements Audited Financials (for turnover above threshold) GST Filings (GSTR-3B, GSTR-1 for last 12 months) | Assesses financial health, turnover, profitability, and repayment capacity. |

| KYC (Know Your Customer) | Aadhaar Card of all Promoters/Directors PAN Card of all Promoters/Directors Passport-size Photographs | Verifies identity and address of key individuals associated with the business. |

| Other Documents (as required) | Business Plan / Project Report Sanction Letters of Existing Loans Ownership Proof of Business Premises | Provides deeper insight into business operations, future plans, and existing liabilities. |

Source: General Lending Practices of Indian Financial Institutions; MSME Ministry Guidelines (msme.gov.in)

Key Takeaways

- Udyam Registration is a vital document, enhancing credibility and eligibility for government-backed collateral-free loan schemes like CGTMSE and MUDRA (refer mudra.org.in).

- Lenders prioritize strong financial health, evidenced by consistent bank statements, ITRs, and GST filings for at least the last 2-3 years.

- A good CIBIL score for both the business and its promoters/directors is critical, directly impacting eligibility and the interest rates offered on unsecured loans.

- Mandatory KYC documents (PAN, Aadhaar) are required for the business entity and all its key managerial personnel for all loan applications.

- Business vintage (typically a minimum of 1-3 years) and consistent turnover are key indicators of operational stability and repayment capability for unsecured lending decisions.

Government Schemes Offering Business Loans Without Collateral

Government schemes like the Pradhan Mantri Employment Generation Programme (PMEGP), Pradhan Mantri Mudra Yojana (PMMY), and the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) offer significant avenues for Indian SMEs to secure business loans without traditional collateral. These initiatives are designed to promote entrepreneurship, facilitate financial inclusion, and mitigate risk for lenders, making credit accessible to a broader base of micro and small enterprises.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

Access to credit remains a pivotal challenge for Micro, Small, and Medium Enterprises (MSMEs) across India. Recognising this barrier, the Indian government has strategically implemented various schemes to facilitate collateral-free business loans, thereby empowering entrepreneurs and fostering economic growth. In the fiscal year 2025-26, these schemes continue to play a crucial role, with an increasing number of MSMEs leveraging them to scale operations, innovate, and create jobs without the burden of pledging personal or business assets.

These government-backed initiatives not only provide financial assistance but also integrate mechanisms to de-risk lending for financial institutions, ensuring a more fluid credit flow to deserving businesses. The schemes are tailored to address different scales of business needs, from new startups seeking initial capital to established small businesses looking for expansion funds.

Key Government Schemes for Collateral-Free Business Loans

Several flagship government programmes specifically target the provision of business loans without demanding collateral. Understanding their specifics is crucial for entrepreneurs.

- Pradhan Mantri Employment Generation Programme (PMEGP): Operated by the Ministry of MSME through Khadi and Village Industries Commission (KVIC), State Khadi and Village Industries Boards (KVIBs), and District Industries Centres (DICs), PMEGP offers financial assistance for setting up new micro-enterprises. The scheme provides a subsidy on the project cost, thereby reducing the loan burden. For manufacturing units, the maximum project cost eligible is Rs 25 lakh, and for service units, it's Rs 10 lakh. Beneficiaries receive a subsidy ranging from 15% to 35% of the project cost, making it an attractive option for first-time entrepreneurs.

- Pradhan Mantri Mudra Yojana (PMMY): Launched by the Prime Minister in 2015, MUDRA provides collateral-free loans up to Rs 10 lakh to non-corporate, non-farm small/micro enterprises. These loans are extended by various financial institutions, including Commercial Banks, Regional Rural Banks (RRBs), Small Finance Banks (SFBs), and Non-Banking Financial Companies (NBFCs). The scheme is categorised into three products: 'Shishu' (loans up to Rs 50,000), 'Kishore' (loans above Rs 50,000 and up to Rs 5 lakh), and 'Tarun' (loans above Rs 5 lakh and up to Rs 10 lakh), catering to different stages of enterprise growth. (Source: mudra.org.in)

- Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE): This scheme provides credit guarantees to Member Lending Institutions (MLIs) for collateral-free credit facilities extended to MSMEs. Established jointly by the Ministry of MSME and SIDBI, CGTMSE ensures that banks can provide loans up to Rs 5 crore without demanding primary or collateral security. The guarantee cover can be up to 85% of the loan amount, significantly de-risking the lending process for financial institutions and thereby encouraging them to lend more freely to MSMEs. The guarantee fee typically ranges from 0.37% to 1.35% per annum, with additional benefits for women entrepreneurs and units in the North Eastern Region. (Source: sidbi.in)

Scheme Benefits Table (2025-26)

| Scheme | Nodal Agency | Benefit/Limit (2025-26) | Eligibility | How to Apply |

|---|---|---|---|---|

| PMEGP | KVIC, KVIB, DIC | Max project cost Rs 25L (Mfg), Rs 10L (Service); Subsidy 15-35% | New projects; 18+ years; No income limit | Online via kviconline.gov.in |

| MUDRA Yojana | Commercial Banks, RRBs, SFBs, NBFCs | Shishu (up to Rs 50K), Kishore (Rs 50K-5L), Tarun (Rs 5L-10L) | Micro/small enterprises in manufacturing, trading, services, allied agri | Direct application at bank branches or online via mudra.org.in |

| CGTMSE | SIDBI | Guarantee up to Rs 5 crore; Fee 0.37-1.35% | New & existing MSMEs; Loans from eligible lending institutions | Through Member Lending Institutions (Banks) (Source: sidbi.in) |

These schemes are instrumental in promoting financial inclusion and entrepreneurship, especially for micro and small enterprises. Udyam Registration (Gazette S.O. 2119(E), 26 June 2020) is often a prerequisite or highly beneficial for accessing the various benefits under these government programmes, streamlining the process of availing support.

Key Takeaways

- Government schemes like PMEGP, MUDRA, and CGTMSE enable Indian SMEs to access business loans without needing to provide traditional collateral.

- PMEGP supports new micro-enterprises with projects up to Rs 25 lakh (manufacturing) and Rs 10 lakh (services), offering a subsidy of 15-35%.

- MUDRA Yojana provides collateral-free loans up to Rs 10 lakh across 'Shishu', 'Kishore', and 'Tarun' categories for micro and small enterprises.

- CGTMSE offers a credit guarantee cover of up to Rs 5 crore to Member Lending Institutions, significantly reducing risk for banks lending to MSMEs.

- These schemes are crucial for financial inclusion and promoting entrepreneurship by making credit accessible to a broader segment of businesses.

2025-2026 Updates: New RBI Guidelines for Unsecured Business Lending

RBI's guidelines for unsecured business lending, with continued emphasis in 2025-2026, primarily focus on strengthening financial stability and promoting prudent risk management by commercial banks. These directives influence how banks assess creditworthiness, set capital adequacy, and manage asset quality across their portfolios, thereby indirectly impacting the availability and terms of collateral-free loans for Indian SMEs. The central bank balances the need for robust credit growth with sound lending practices.

Updated 2025-2026: The Reserve Bank of India (RBI) continues its proactive approach to prudential supervision, with ongoing refinements to risk weight norms and credit appraisal frameworks impacting unsecured lending portfolios for banks. This builds upon previous circulars emphasizing robust internal risk assessment and capital adequacy for balanced credit growth, as detailed in various RBI circulars on prudential norms.

Indian SMEs often face challenges in securing collateral-backed loans, making unsecured options vital for their sustained growth and operational flexibility. In 2025-2026, the demand for such credit continues to expand, with many small businesses seeking agile financial support to capitalize on market opportunities. The Reserve Bank of India (RBI), as the apex banking regulator, plays a pivotal role in shaping the landscape of unsecured business lending through its comprehensive regulatory and supervisory oversight, aiming to ensure both financial system stability and adequate credit flow to the productive sectors of the economy.

Under the powers vested by the RBI Act 1934, the central bank issues guidelines that govern all aspects of commercial banking operations, including lending. While there aren't specific 'unsecured loan' guidelines in isolation, RBI's broader framework on prudential norms, risk management, and capital adequacy directly impacts how banks approach collateral-free lending. These norms ensure that banks maintain healthy balance sheets and are resilient to potential credit defaults.

A key area of RBI's influence lies in its directives on asset classification, income recognition, and provisioning (IRACP) norms. These guidelines dictate how banks categorize loans, recognize interest income, and set aside provisions for potential losses. For unsecured loans, which inherently carry a higher risk profile, banks are often required to maintain higher provisions if asset quality deteriorates. This compels banks to adopt rigorous credit appraisal processes for unsecured advances, ensuring borrowers have strong repayment capacities and sound business models.

Furthermore, RBI's framework, aligned with global Basel norms for capital adequacy, assigns risk weights to different types of assets held by banks. Unsecured exposures, by their very nature, typically attract higher risk weights compared to secured loans. This means that banks need to allocate a greater amount of their capital against unsecured loans to meet their minimum capital adequacy ratio (CAR). Consequently, banks must carefully balance their unsecured lending portfolios to optimize capital utilization and maintain regulatory compliance. This mechanism directly influences a bank's capacity and willingness to extend collateral-free credit.

The RBI also continuously monitors the overall asset quality of the banking system. Concerns over rising non-performing assets (NPAs), particularly in segments perceived as higher risk such as unsecured retail or business loans, often prompt the central bank to issue advisories. These advisories typically urge banks to further strengthen their internal risk management systems, enhance credit appraisal mechanisms, improve monitoring of borrower accounts, and bolster recovery processes. Such proactive measures, while aimed at system-wide stability, can lead to banks becoming more cautious in their unsecured lending practices, influencing loan terms and eligibility criteria for SMEs.

Impact on SME Collateral-Free Credit Access

While RBI's guidelines set the broad regulatory environment, specific government-backed initiatives like the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) and the Pradhan Mantri MUDRA Yojana (MUDRA) directly facilitate collateral-free loans for SMEs. These schemes operate within the RBI-regulated banking system, providing guarantees or refinance support to banks, thereby mitigating a significant portion of the default risk. RBI's regulatory framework ensures that banks participating in these schemes adhere to sound lending, reporting, and compliance practices, contributing to the schemes' overall effectiveness and integrity.

Moreover, the Reserve Bank's monetary policy decisions, such as adjustments to the repo rate, have a significant bearing on the cost of funds for banks. Changes in the repo rate directly influence the interest rates that banks offer on various loan products, including unsecured business loans. A higher repo rate can lead to increased borrowing costs for SMEs seeking collateral-free credit, potentially affecting their project viability and overall demand for such loans. Therefore, the RBI's ongoing vigilance and adaptive regulatory approach are critical in shaping the availability, cost, and overall prudence of unsecured business lending for Indian SMEs.

Key Takeaways

- RBI's prudential norms for asset classification and provisioning guide banks' risk management for all loans, including unsecured ones, ensuring financial stability.

- Unsecured loans typically attract higher risk weights under RBI's capital adequacy framework, compelling banks to allocate more capital against them.

- The RBI continuously monitors banks' asset quality, issuing advisories that influence their approach to unsecured credit growth and risk assessment.

- Government-backed schemes like CGTMSE and MUDRA facilitate collateral-free loans for SMEs, operating under the regulatory oversight of the RBI-regulated banking system.

- Monetary policy decisions by the RBI, such as changes in the repo rate, directly affect the overall cost and availability of unsecured business credit for SMEs.

Bank-wise and NBFC Comparison: Interest Rates and Loan Amounts

For collateral-free business loans, banks typically offer lower interest rates and higher loan amounts, often through government-backed schemes like MUDRA and CGTMSE, but with stricter eligibility and longer processing times. NBFCs, conversely, provide quicker disbursals and more flexible criteria for their proprietary unsecured loans, albeit generally at higher interest rates and for slightly lower maximum amounts.

In the financial landscape of 2025-26, the demand for collateral-free business loans among Indian Small and Medium Enterprises (SMEs) has surged, driven by growth ambitions and government impetus. This growing segment, crucial for India's economic resilience, often finds itself navigating a diverse set of options from both traditional banks and Non-Banking Financial Companies (NBFCs) for unsecured funding.

Collateral-free loans for SMEs primarily fall into two categories: government-backed schemes channelled through various financial institutions, and proprietary unsecured loan products offered directly by banks and NBFCs. Schemes like the Pradhan Mantri Mudra Yojana (PMMY) are designed for micro-enterprises, providing loans up to Rs 10 lakh, while the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) scheme covers term loans and working capital facilities up to Rs 5 crore without collateral, primarily disbursed by banks and select NBFCs. Mudra.org.in and sidbi.in are official portals for details on these.

Interest rates for these loans are influenced by several factors, including the Reserve Bank of India's (RBI) repo rate, the applicant's creditworthiness, business vintage, and the loan's tenure. For government-backed schemes, rates are often capped or subsidised to promote MSME growth. For proprietary unsecured loans, lenders assess risk based on factors such as credit score (CIBIL), cash flow, and industry risk, leading to varying rates.

Comparison of Banks and NBFCs for Collateral-Free Loans

Here’s a comparative overview:

- Public Sector Banks (PSBs): Generally offer the most competitive interest rates, often starting lower than private banks or NBFCs. They are major implementing agencies for schemes like MUDRA (Shishu up to Rs 50,000, Kishore Rs 50,000 to Rs 5 lakh, Tarun Rs 5 lakh to Rs 10 lakh) and CGTMSE (up to Rs 5 crore). While their processing times can be longer and documentation stricter, their emphasis on priority sector lending makes them a strong choice for eligible MSMEs.

- Private Sector Banks (PVBs): Offer a balance between competitive rates and faster processing compared to PSBs. They also participate in government schemes but may have more aggressive targets for their own unsecured business loan products, typically extending up to Rs 75 lakh or even Rs 1 crore based on robust financial health and a strong credit score.

- Non-Banking Financial Companies (NBFCs): Renowned for their agility, NBFCs provide quicker loan approvals and disbursals, making them ideal for businesses with urgent funding needs. They often have more flexible eligibility criteria than banks, sometimes accepting newer businesses or those with less perfect credit histories. However, this flexibility comes at a cost; NBFC interest rates are generally higher, reflecting their higher risk appetite and operational costs. Loan amounts can range up to Rs 50-75 lakh for unsecured products.

The choice between a bank and an NBFC depends largely on the borrower's specific needs—whether priority is given to the lowest interest rate, fastest disbursal, or more flexible eligibility.

| Lender Type | Loan Scheme / Category | Typical Interest Rate (p.a.) (2025-26) | Max Collateral-Free Loan Amount | Key Characteristics |

|---|---|---|---|---|

| Public Sector Bank | MUDRA Shishu/Kishore/Tarun | 8.00% - 15.00% | Up to Rs 10 Lakh (MUDRA Tarun) | Focus on micro-enterprises, priority sector lending, lower rates |

| Public Sector Bank | CGTMSE Backed Term Loan | 9.00% - 14.00% | Up to Rs 5 Crore | Government guarantee, for eligible MSMEs, longer processing |

| Private Sector Bank | Unsecured Business Loan | 10.00% - 18.00% | Up to Rs 75 Lakh - Rs 1 Crore | Faster processing, good credit score essential, broader eligibility |

| NBFC | Unsecured Business Loan | 12.00% - 24.00% | Up to Rs 50 Lakh - Rs 75 Lakh | Flexible eligibility, quick disbursal, higher risk appetite, higher rates |

Source: MUDRA (mudra.org.in), CGTMSE (sidbi.in), general market trends for unsecured loans (April 2026)

Key Takeaways

- Public Sector Banks offer the lowest interest rates for collateral-free loans, often through government schemes like MUDRA (up to Rs 10 lakh) and CGTMSE (up to Rs 5 crore).

- Private Sector Banks provide a balance of competitive rates and relatively quicker processing for unsecured loans up to Rs 75 lakh to Rs 1 crore.

- NBFCs offer faster disbursal and more flexible eligibility criteria, but generally at higher interest rates, typically for loan amounts up to Rs 50-75 lakh.

- Government schemes like PMMY and CGTMSE are crucial avenues for MSMEs seeking collateral-free funding, with defined limits and criteria.

- Interest rates for unsecured loans are influenced by RBI's repo rate, borrower creditworthiness, and the specific lender's risk assessment.

Common Mistakes When Applying for Unsecured Business Loans

Entrepreneurs often make critical errors when seeking unsecured business loans, such as neglecting to maintain a strong credit score, submitting incomplete documentation, or failing to understand lender-specific eligibility criteria. Misrepresenting financial information or not leveraging MSME status, particularly Udyam registration, can significantly reduce approval chances and lead to rejection.

In the competitive landscape of 2025-26, Indian SMEs are increasingly seeking unsecured business loans to fuel growth and manage working capital, with a notable surge in demand post-economic shifts. However, securing these collateral-free funds requires meticulous preparation. Many businesses, despite their potential, fall short due to common, avoidable mistakes that could otherwise lead to successful loan approval.

- Neglecting Credit Score and Financial History: Lenders heavily rely on the applicant's credit score (CIBIL, Experian, etc.) and the business's financial history to assess creditworthiness for unsecured loans. A low credit score, frequent loan defaults, or erratic repayment patterns signal high risk. It's crucial for proprietors and businesses to maintain a healthy credit profile, as lenders review both personal and business credit scores for proprietorships and partnerships. Regular monitoring and timely repayment of existing obligations are essential for a good standing.RBI Guidelines

- Submitting Incomplete or Inaccurate Documentation: A common pitfall is providing an incomplete set of documents or submitting information that is inconsistent or incorrect. Unsecured loans demand a thorough review of financial statements (Profit & Loss, Balance Sheet), bank statements (past 6-12 months), GST returns (if applicable), and business registration proofs (e.g., Udyam Registration Certificate). Any discrepancy or missing document can cause significant delays or outright rejection. For MSMEs, possessing a valid Udyam registration certificate is often a prerequisite for many government-backed schemes and priority sector lending benefits.Udyam Registration Portal

- Not Understanding Eligibility Criteria: Each lender and loan product has specific eligibility requirements concerning business vintage, minimum turnover, profitability, and geographic location. Many applicants apply without thoroughly reviewing these criteria, leading to wasted effort. For instance, schemes like MUDRA loans (up to Rs 10 lakh) or PMEGP (up to Rs 25 lakh for manufacturing) have distinct conditions regarding business type, project cost, and borrower profile. Understanding these nuances before applying is vital.Mudra.org.in

- Lack of a Robust Business Plan or Purpose: While not always a mandatory document, a well-articulated business plan demonstrating financial projections, market analysis, and a clear purpose for the loan can significantly strengthen an application. Lenders prefer to understand how the funds will be utilized and how the business intends to generate revenue to repay the loan. A vague or poorly structured plan raises doubts about the business's viability and repayment capacity.Startup India Guidelines

- Applying to Too Many Lenders Simultaneously: While it might seem strategic, applying for loans with multiple lenders within a short period can negatively impact your credit score. Each loan application often triggers a "hard inquiry" on your credit report, which can temporarily lower your score. A series of such inquiries suggests financial distress and can make lenders hesitant to approve your application. It's advisable to research thoroughly and apply to a select few lenders where eligibility is highly likely.RBI Regulations

- Ignoring Terms and Conditions: Many borrowers overlook the fine print of loan agreements, including interest rates, processing fees, repayment schedules, and penalty clauses for late payments. This oversight can lead to unexpected costs or difficulties in managing repayments. It's crucial to understand the total cost of the loan and its implications for cash flow before signing any agreement.Ministry of Finance

- Not Leveraging MSME Status: For eligible businesses, obtaining Udyam Registration is a strategic advantage. Registered MSMEs (Micro, Small, and Medium Enterprises) are prioritized for many government schemes, benefit from easier access to credit, and enjoy certain interest rate concessions. Failing to highlight or even obtain this crucial certification can mean missing out on significant benefits designed to support small businesses in India. The MSMED Act 2006, along with subsequent notifications, underpins many of these advantages.MSME Ministry

Key Takeaways

- Maintain a strong personal and business credit score for higher chances of unsecured loan approval.

- Ensure all documentation is complete, accurate, and consistent to avoid application delays or rejections.

- Thoroughly research and understand each lender's specific eligibility criteria and loan terms before applying.

- Develop a clear, comprehensive business plan and avoid excessive simultaneous loan applications.

- Leverage MSME status through Udyam Registration to access priority sector lending and other government benefits.

Real-world Case Studies: Successful Unsecured Loan Applications

Indian SMEs successfully secure unsecured loans primarily by leveraging government-backed schemes like MUDRA, CGTMSE, and PMEGP, which offer collateral-free credit for various business needs. Approval often depends on robust business plans, consistent financial performance, and compliance with scheme-specific eligibility criteria, especially Udyam Registration.

In the dynamic Indian business landscape of 2025-26, access to finance remains crucial for MSME growth. A recent trend indicates that over 70% of new MSME loans are now availed without traditional collateral, thanks to enhanced government support and digital lending platforms. Understanding how real businesses navigate this process provides invaluable insights for aspiring entrepreneurs seeking collateral-free funding.

Unsecured business loans are a boon for micro, small, and medium enterprises (MSMEs) that lack substantial assets to pledge as security. These loans are often facilitated through government schemes designed to boost entrepreneurship and employment. Successful applications typically demonstrate a clear business objective, sound financial health, and adherence to regulatory requirements, particularly Udyam Registration, which acts as a gateway to many benefits (udyamregistration.gov.in).

Case Study 1: Micro-Enterprise Boosted by MUDRA Shishu Loan

Business: “Kisan Fresh Foods,” a small food processing unit in rural Maharashtra specializing in packaged traditional snacks, started by Ms. Priya. She had a robust business idea and local demand but lacked capital for initial equipment and raw materials.

- Challenge: Ms. Priya needed approximately ₹40,000 to purchase a commercial mixer, packaging machine, and initial stock. She had no collateral.

- Solution: She applied for a Shishu loan under the Pradhan Mantri MUDRA Yojana (PMMY) through a regional rural bank. The Shishu category provides loans up to ₹50,000 (mudra.org.in). She presented a simple business plan outlining her product, market, and revenue projections.

- Outcome: Her loan was approved within two weeks due to a clear proposal and good local credit history. The funds enabled her to procure essential machinery and begin production, significantly increasing her capacity and market reach. Kisan Fresh Foods now employs 3 local women.

Case Study 2: Small Manufacturing Unit Leveraging CGTMSE

Business: “TechFab Solutions,” a small-scale textile manufacturing unit in Gujarat, run by Mr. Anil. Established for three years, the unit manufactured specialized technical fabrics for industrial use. They wanted to upgrade machinery to meet growing demand and diversify their product line, requiring significant capital.

- Challenge: TechFab Solutions needed a term loan of ₹1.5 crore for new automated looms and working capital. While profitable, their existing assets were fully leveraged, leaving no additional collateral for a new loan.

- Solution: Mr. Anil, whose unit was Udyam Registered as a 'Small' enterprise, approached a public sector bank. The bank assessed their financial statements, consistent order book, and growth projections. Recognizing the collateral challenge, the bank recommended applying for the loan under the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) scheme (sidbi.in). CGTMSE provides credit guarantees up to ₹5 crore for eligible MSMEs without requiring collateral from the borrower.

- Outcome: The ₹1.5 crore loan was approved with CGTMSE coverage, removing the need for collateral. This allowed TechFab Solutions to acquire modern machinery, enhance production efficiency, and expand into new markets, doubling its annual turnover in the subsequent year. The CGTMSE fee, typically 0.37-1.35% of the guaranteed amount, was factored into the loan structure.

Case Study 3: Service Sector Startup Utilizing PMEGP

Business: “DigiInnovate,” a new IT and digital marketing services startup in Uttar Pradesh, founded by Ms. Ritu and her team of young graduates. They aimed to provide affordable digital solutions to local SMEs but lacked initial funding for office space, computers, and marketing.

- Challenge: Ms. Ritu's team had innovative ideas but no prior business history or collateral to secure a startup loan. They needed about ₹8 lakh to set up operations.

- Solution: They identified the Prime Minister's Employment Generation Programme (PMEGP) as a suitable option. PMEGP aims to generate employment opportunities by establishing micro-enterprises in non-farm sectors, offering financial assistance through banks with a substantial subsidy (kviconline.gov.in). The maximum project cost for services under PMEGP is ₹10 lakh. After preparing a detailed project report and undergoing entrepreneurship development training (EDP), they applied for the loan through a nationalized bank.

- Outcome: The loan of ₹8 lakh was sanctioned, accompanied by a significant subsidy (up to 35% for special categories/regions, 15-25% for general) on the project cost. This reduced their effective loan burden and allowed DigiInnovate to successfully launch their services, acquiring several local clients and creating employment for five individuals.

Key Takeaways

- Government schemes like MUDRA, CGTMSE, and PMEGP are primary avenues for Indian SMEs to secure collateral-free loans, catering to diverse business needs and sizes.

- Udyam Registration is a crucial prerequisite for accessing many MSME-specific benefits and schemes, simplifying the application process.

- A well-prepared business plan, demonstrating viability and growth potential, significantly improves the chances of unsecured loan approval.

- Even without collateral, lenders assess the borrower's credit history, financial health, and repayment capacity.

- Entrepreneurs should research and align their funding needs with the specific criteria of each scheme to maximize their success rate.

Unsecured Business Loan Frequently Answered Questions

Unsecured business loans, vital for many Indian SMEs, are evaluated based on factors like credit score, business vintage, turnover, and existing financial health rather than collateral. Approval rates are influenced by the applicant's creditworthiness and the lender's risk assessment, with interest rates typically ranging higher than secured loans due to the increased risk. Government schemes like MUDRA and CGTMSE significantly enhance access to collateral-free finance, offering loans up to ₹10 lakh and guarantees up to ₹5 crore respectively.

In the dynamic Indian business landscape, unsecured business loans have become a crucial financial instrument for Micro, Small, and Medium Enterprises (MSMEs) seeking growth capital without pledging assets. With the Indian economy projected for robust growth, access to timely and flexible finance is paramount. In 2025-26, the demand for collateral-free credit continues to rise as businesses expand operations, invest in technology, and manage working capital efficiently.

What factors influence unsecured business loan approval rates?

Several key factors determine the approval of an unsecured business loan. Lenders primarily assess the applicant's creditworthiness, which includes a strong CIBIL score for both the business and its promoters. Business vintage, typically requiring a minimum of 1-3 years of operation, and consistent annual turnover demonstrating repayment capacity are also critical. A healthy debt-to-equity ratio and profitability are also closely scrutinized. Lenders often prefer businesses with stable cash flows and a clear business plan for utilizing the funds.

What are the typical interest rates for unsecured business loans?

Unsecured business loans generally carry higher interest rates compared to secured loans due to the absence of collateral, which increases the lender's risk. While specific rates vary significantly between lenders and depend on the borrower's risk profile, they typically range from 11% to 24% per annum. Factors such as the loan amount, repayment tenure, credit score, and the lender's internal policies all play a role in determining the final interest rate offered. Government-backed schemes might offer more competitive rates or subsidies.

What is the maximum loan amount one can obtain without security?

The maximum loan amount for unsecured business loans varies widely. Under the Pradhan Mantri Mudra Yojana (PMMY), businesses can access up to ₹10 lakh in collateral-free loans, categorized as Shishu (up to ₹50,000), Kishore (₹50,001 to ₹5 lakh), and Tarun (₹5 lakh to ₹10 lakh) as per mudra.org.in. For higher amounts, the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) scheme guarantees collateral-free loans up to ₹5 crore from eligible financial institutions, enabling SMEs to access substantial credit without security (sidbi.in). Other private lenders might offer higher amounts based on business financials.

What is the typical repayment tenure for such loans?

Repayment tenures for unsecured business loans are generally shorter than secured loans, typically ranging from 12 months to 60 months (1 to 5 years). The exact tenure depends on the loan amount, the borrower's repayment capacity, and the lender's policy. Shorter tenures result in higher monthly EMIs but less overall interest paid, while longer tenures reduce monthly burden but increase the total interest outgo. Under PMMY, the repayment period can extend up to 5 years, aligning with this common range.

Are there any specific government schemes that offer unsecured loans?

Yes, the Indian government has several robust schemes to facilitate collateral-free financing for MSMEs. The flagship Pradhan Mantri Mudra Yojana (PMMY) offers loans up to ₹10 lakh for micro-enterprises. The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) provides a guarantee cover to banks for collateral-free loans up to ₹5 crore sanctioned to MSMEs, reducing the risk for lenders and encouraging them to extend credit (sidbi.in). Additionally, the Prime Minister's Employment Generation Programme (PMEGP) offers subsidies on project costs for new enterprises, which can indirectly assist in obtaining unsecured financing for manufacturing projects up to ₹25 lakh and service projects up to ₹10 lakh.

Can a new business get an unsecured loan?

While challenging, it is possible for new businesses to obtain unsecured loans, especially under specific government schemes. The Shishu category of the MUDRA loan is specifically designed for startups and micro-enterprises, providing up to ₹50,000. Lenders may also consider strong business plans, the promoter's educational background and industry experience, and any initial capital injection. Additionally, specific startup initiatives under the Startup India program might offer avenues for funding, though not always directly as traditional unsecured loans.

What documentation is generally required for unsecured business loans?

Common documentation includes KYC documents for the business and its promoters (PAN, Aadhaar), business registration proofs (Udyam Registration Certificate, GSTIN if applicable), bank statements (typically for the last 6-12 months), and financial statements such as audited balance sheets, profit & loss statements, and Income Tax Returns (ITR) for the past 2-3 years. For newer businesses or smaller loan amounts under MUDRA, documentation requirements might be simpler, focusing on basic identity and business proof.

Key Takeaways

- Unsecured business loan approval heavily relies on creditworthiness, business vintage (1-3 years minimum), and consistent turnover, rather than physical collateral.

- Interest rates for collateral-free loans are generally higher, typically ranging from 11% to 24% annually, reflecting the increased risk for lenders.

- Government schemes like Pradhan Mantri Mudra Yojana (PMMY) offer collateral-free loans up to ₹10 lakh, while CGTMSE provides guarantees for loans up to ₹5 crore to MSMEs (sidbi.in).

- Repayment tenures usually span 1 to 5 years, with the specific period influenced by the loan amount and the borrower's financial capacity.

- New businesses can secure unsecured loans, particularly through schemes like MUDRA's Shishu category, by presenting a robust business plan and demonstrating promoter capability.

- Essential documentation includes KYC for business and promoters, business registration proofs (Udyam, GSTIN), bank statements, and financial statements (ITR, P&L, balance sheet).

Conclusion and Official Resources for Business Loan Applications

Collateral-free business loans are pivotal for fostering entrepreneurship and growth among Indian SMEs, particularly new and micro-enterprises that may lack tangible assets. Government schemes like Pradhan Mantri MUDRA Yojana, the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), and the Prime Minister's Employment Generation Programme (PMEGP) are primary mechanisms for extending such financial support without requiring traditional security, thereby enhancing credit access.

Important: Udyam Registration at udyamregistration.gov.in is completely free of charge as per Gazette S.O. 2119(E), 26 June 2020. No fee is charged at any stage.

Indian Micro, Small, and Medium Enterprises (MSMEs) continue to be the backbone of the nation's economy, contributing significantly to GDP, innovation, and employment generation. In 2025-26, the focus on empowering these enterprises through accessible finance, especially collateral-free loans, remains paramount. Many emerging businesses and startups often face challenges in securing traditional loans due to a lack of collateral, a barrier that government-backed schemes are specifically designed to overcome. These initiatives aim to democratize access to credit, ensuring that promising business ideas are not stifled by financial constraints.

The Pradhan Mantri MUDRA Yojana (PMMY), operational since 2015, stands as a cornerstone for micro-enterprises, offering loans up to Rs 10 lakh in three categories – Shishu (up to Rs 50,000), Kishore (Rs 50,000 to Rs 5 lakh), and Tarun (Rs 5 lakh to Rs 10 lakh) – without requiring collateral. This has significantly boosted small-scale entrepreneurship across various sectors. Furthermore, the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), managed by SIDBI, provides a credit guarantee cover to banks for collateral-free loans extended to MSMEs, up to Rs 5 crore. This mechanism de-risks lending for financial institutions, encouraging them to provide more credit to eligible MSMEs, including new and existing businesses for working capital or term loans. The guarantee fee typically ranges from 0.37% to 1.35% of the loan amount, with additional concessions for women entrepreneurs and units in the North-Eastern Region.

For entrepreneurs looking to set up new projects, the Prime Minister's Employment Generation Programme (PMEGP) offers financial assistance in the form of subsidies on project costs, facilitating loans up to Rs 25 lakh for manufacturing units and Rs 10 lakh for service units. While not strictly a collateral-free loan program itself, the subsidy component significantly reduces the loan burden and, combined with CGTMSE, often enables entrepreneurs to secure the remaining financing without pledging personal assets. A crucial prerequisite for accessing most of these MSME-specific benefits, including collateral-free loans and priority sector lending, is obtaining Udyam Registration, which can be done entirely free of charge on the official udyamregistration.gov.in portal as per Gazette Notification S.O. 2119(E) dated 26 June 2020. This registration categorizes businesses as Micro, Small, or Medium based on investment and turnover criteria, opening doors to a plethora of governmental support. Businesses without PAN and GSTIN can also register through the Udyam Assist Platform (udyamassist.gov.in), launched in January 2023, catering to informal micro units.

Key Official Resources for Applications

- Udyam Registration: For obtaining the essential Udyam Certificate and classifying your enterprise as MSME. (udyamregistration.gov.in)

- Pradhan Mantri MUDRA Yojana (PMMY): For micro-enterprises seeking collateral-free loans up to Rs 10 lakh. (mudra.org.in)

- Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE): To understand the credit guarantee scheme for collateral-free loans up to Rs 5 crore. (sidbi.in)

- Prime Minister's Employment Generation Programme (PMEGP): For entrepreneurs seeking subsidies on new project costs. (kviconline.gov.in)

- Government e-Marketplace (GeM): For MSMEs to participate in government procurement, often with exemptions like Earnest Money Deposit (EMD) as per GFR Rule 170, requiring Udyam registration. (gem.gov.in)

Key Takeaways

- Collateral-free loans are crucial for Indian SMEs, especially micro and new enterprises, to overcome financing hurdles.

- Government schemes like MUDRA Yojana, CGTMSE, and PMEGP are the primary sources for such unsecured funding.

- Udyam Registration is a mandatory and free process to avail most MSME-specific benefits, including access to collateral-free credit.

- The CGTMSE scheme can guarantee loans up to Rs 5 crore for MSMEs, significantly reducing risk for lenders.

- Official portals like mudra.org.in and kviconline.gov.in serve as direct application points for these government initiatives.

For comprehensive guidance on Indian business registration and financial topics, UdyamRegistration.Services (udyamregistration.services) provides free, regularly updated guides for entrepreneurs and investors across India.